Wall Street itself rarely issues sell calls. Bank of America stock analysts almost never use the word “sell.” On June 5, they did. Seven of their ten bear market indicators have now fired, matching the average seen ahead of every major peak since 1990. But this is not cynicism. It is the structural reality of how the stock market works. Research arms exist, in part, to support the business of distributing securities to investors. Telling clients to exit the market is bad for that business. Which is why when Savita Subramanian, Bank of America’s head of U.S. equity and quantitative strategy, published a note on June 5 with the title “Too many red flags. Take profits,” it was worth reading carefully.

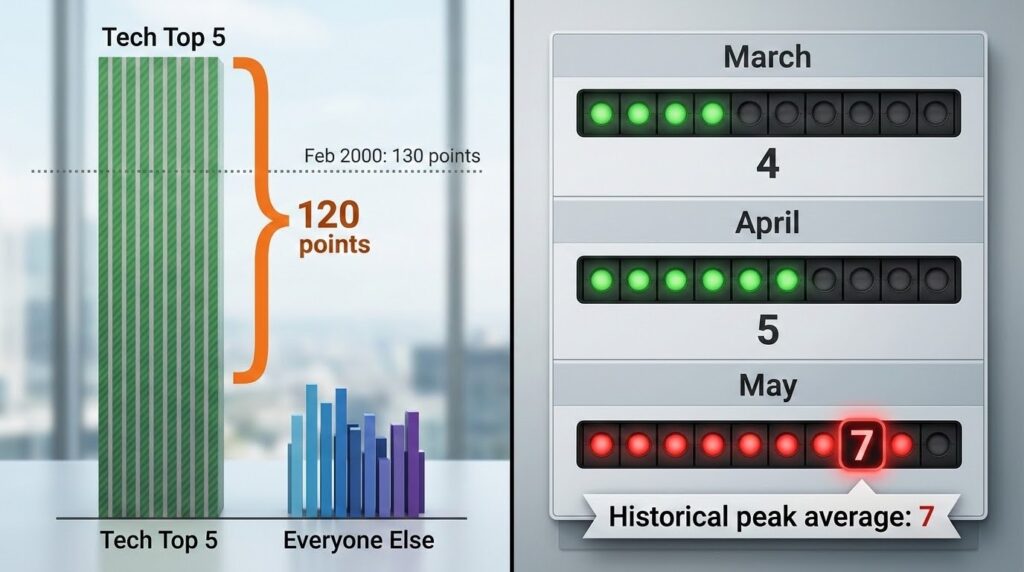

The note was not vague. Seven of the ten internal bear market signposts the bank tracks are now triggered. That count rose from four in March to five in April to seven in May. Seven is the average number of signposts that have been active ahead of every major S&P 500 peak since 1990. The bank’s year-end target of 7,100 implies roughly a 6% decline from where the index closed on Monday.

That is the news. The rest of this article is the translation.

What Are Bank of America Bear Market Signposts and What Do They Measure?

Seven of Bank of America’s ten bear market signposts are now triggered, matching the average count observed before every major S&P 500 peak since 1990.

The ten signposts are not vibes. They are quantifiable market conditions that have historically clustered ahead of peaks. Here are all seven that are currently active.

- First, long-term earnings growth expectations for the S&P 500 have risen significantly above their five-year average. Investors are pricing in above-trend growth. When that growth does not materialize, multiples compress fast.

- Second, credit conditions remain unusually easy. Cheap and available credit has been one of the main engines of the rally. Easy money historically peaks before markets do.

- Third, the Federal Reserve’s Senior Loan Officer Opinion Survey, the SLOOS, showed in May that consumer loan demand continued to soften. Banks are tightening standards even as equity prices remain elevated. The fuel that easy credit provided is beginning to narrow.

- Fourth, consumer confidence has deteriorated. The gap between high equity prices and weakening consumer sentiment has historically closed in one direction.

- Fifth, merger and acquisition activity has surged. Dealmaking booms are a late-cycle indicator. Companies pay peak prices for acquisitions when confidence is highest. Historically, that confidence peaks close to when prices do.

- Sixth, stocks with high price-to-earnings ratios are leading those with low multiples by a wide margin. BofA called this a sign of excessive speculation. When investors stop caring what they pay relative to earnings, they are no longer investing. They are betting.

- Seventh, the two signposts that tipped the count from five to seven in May: the spread between the best and worst performing quintiles within the S&P 500’s technology sector hit 120 percentage points, the widest since February 2000. BofA also flagged that the gap between the top and bottom-performing tenths of the entire S&P 500 jumped to a post-COVID-era high over the past three months. The index is rising, but the gains are sitting in an increasingly narrow band of names.

That last point is what Subramanian meant when she wrote: “We see opportunity in S&P 500 stocks, but not the overall cap-weighted index.” She is not calling the market worthless. She is saying the index has become a bet on whoever is already winning, and that is a structurally different risk than owning the market broadly.

The 3 Signposts That Have Not Fired Yet

Three indicators remain untriggered, and their absence is precisely why BofA said “take profits” rather than “get out.”

- The first is a formal yield curve inversion. The spread between 2-year and 10-year Treasury yields has narrowed to 39 basis points, the tightest level since equivalent tariffs were imposed, per BofA’s note as reported by Multibagg AI. The curve is compressing. It has not inverted. That distinction matters because inversion is historically one of the most reliable recession signals in the framework.

- The second is a formal Sell Side Indicator trigger. The SSI measures average equity allocations recommended by Wall Street strategists. BofA’s own June 5 note explicitly stated that the SSI has not officially triggered despite a sharp deterioration in May. The formal threshold sits near 59%. It’s close, but it hasn’t crossed.

- The third is earnings revision deterioration. BofA acknowledged that the S&P 500’s year-to-date gain has been driven primarily by earnings revisions and not by multiple expansion. Valuation multiples have actually compressed slightly. As long as earnings estimates keep rising, this signpost stays dark.

These three absences draw the line between caution and alarm. Bank of America stock is at the caution line. The market crosses into alarm territory if the curve inverts, earnings estimates start falling, or the SSI pushes past 59%.

Why Is the Tech Sector Dispersion Reading So Unusual?

The gap between the best and worst performing tech stocks hit 120 percentage points in May, a level not seen since February 2000.

The dot-com comparison in the BofA note is not decorative. The February 2000 reading reached 130 percentage points. The S&P 500 peaked on March 24, 2000. Subramanian named that date explicitly.

This does not mean a crash is coming in the next 30 days. It means the gains inside the technology sector have become extraordinarily concentrated in a small number of names, while the rest of the sector lags badly. When a handful of stocks carry an entire index higher, the index valuation stops representing what most stocks are actually worth.

The S&P 500 screens expensive on 17 of 20 valuation metrics BofA tracks and trades above its dot-com bubble-era metrics on eight of them. Strong index performance has, in Subramanian’s words, “masked internal drama.”

What Does Bank of America Stock’s Year-End Target of 7,100 Actually Signal for the Market?

Bank of America stock’s year-end target of 7,100 implies a 6% decline from current levels, not a crash, but a meaningful correction in a concentrated index.

A year-end target of 7,100 on an index currently trading near 7,600 implies a 6% decline by December. That is not a crash. The S&P 500 fell 2.6% the Friday the note dropped, its worst single session since October. In one day, the market covered roughly 40% of the implied full-year downside BofA is forecasting.

The call is not “exit equities.” The call is “reduce excess concentration in whatever has already run the most.” Those are different instructions.

For context on what staying invested through sell signals has historically cost and saved: the data on buying at any price, including at elevated sentiment, shows that systematic purchasing outperforms market timing in approximately 70% of historical periods. The average maximum drawdown following prior BofA sell signals has been 8.5%. That is the historical cost of ignoring this kind of warning and staying put.

That 8.5% figure matters. It is survivable for investors with long-term horizons who will not panic-sell when the drawdown arrives. It is less survivable for investors who discover they cannot tolerate watching their balance drop and end up selling at the worst possible moment. The gap between the return a strategy produces in theory and what an investor actually earns depends entirely on whether they hold through that drawdown. For a rigorous look at the historical data behind that gap, Nick Maggiulli’s Just Keep Buying is the most data-driven treatment available.

Who Should Act on the Bank of America Stock Warning and Who Can Safely Ignore It?

The risk for pre-retirees is not an abstract loss. It is being forced to sell equities at a drawdown to fund a known, dated spending event.

The BofA warning does not deliver the same instruction to every investor.

- If you are in the accumulation phase with 15 or more years before a major withdrawal event, the signal does not require action. The average maximum drawdown following this type of signal is 8.5%. A diversified, long-horizon portfolio absorbs that. Exiting, waiting, and re-entering historically costs more in missed compounding than the correction avoids.

- If you are within five years of retirement or within three years of a major planned capital event, a business sale, a home purchase, a college tuition cycle, the picture is different. Seven of ten signposts firing at the historical average for prior market peaks is not noise to dismiss at that stage of a plan. The specific risk is not losing money in the abstract. It is being forced to sell equities at a loss to fund a known, dated spending need. That is the sequence-of-returns problem, and it is exactly what this type of market environment creates.

- If you hold a concentrated position in AI-era technology companies through an index fund, re-read Subramanian’s sentence: “not the overall cap-weighted index.” BofA is not warning about the market broadly. They are warning about the structure of what the index has become. An S&P 500 index fund today is significantly a bet on a small number of technology names. The tech sector dispersion data says those names have already done most of their running while the rest of the sector has lagged behind. That concentration is the specific risk being flagged.

None of this is a prediction. It is a reading of the conditions that have historically preceded peaks, applied to your actual situation.

For educational purposes only. Not financial advice. Researched and fact-checked by the TheCapitalist.com editorial team using a multi-source framework. Institutional citations verified. Contradictory expert positions represented. See our editorial standards.

Frequently Asked Questions

What is Bank of America stock’s Sell Side Indicator and why does it matter?

The Sell Side Indicator tracks the average equity allocation recommended by Wall Street strategists. It functions as a contrarian tool. Extreme strategist optimism has historically preceded pullbacks. As of early 2026, the indicator remained near multi-year highs and within approximately two percentage points of triggering a formal sell threshold.

Does BofA’s warning mean the stock market is about to crash?

No. BofA’s year-end target of 7,100 implies roughly a 6% decline, not a crash. Their specific instruction was to reduce exposure to the cap-weighted index, not exit equities entirely. The distinction matters for how investors respond.

What are the bear market signposts BofA triggered?

BofA tracks ten market-condition indicators that have historically clustered before S&P 500 peaks. Seven are now active, up from five in April and four in March, matching the average count observed before every major peak since 1990. The triggers include growth expectations, tech dispersion, credit conditions, high P/E speculation, consumer confidence deterioration, M&A activity, and market breadth deterioration.

Should long-term investors sell based on this warning?

It depends on the timeline and portfolio composition. Investors with 15 or more years before a major withdrawal event have historically absorbed similar signals without needing to act. Investors within five years of retirement or a large planned expenditure face more concentrated sequence-of-returns risk and have stronger reason to review their equity exposure now.