The number everyone in finance has been circling for months is $725 billion. That is the combined amount Amazon, Alphabet, Microsoft, Meta, and Oracle have committed to AI infrastructure spending in 2026. To put that in context: Amazon’s $200 billion share alone exceeds the combined annual capital expenditure of the entire publicly traded United States energy sector. The Big Four (Amazon, Alphabet, Meta, and Microsoft) increased their capital expenditures by more than 60 percent from already historic 2025 levels. And critically, they are no longer funding all of it from cash.

That last part is what changes the investor calculus.

For most of the cloud era, these were cash-generating machines. They built data centers from operating profits, returned billions to shareholders through buybacks, and carried conservative balance sheets that made them look more like utilities than growth companies. That model ended quietly in late 2024. Since then, the five largest hyperscalers have tapped capital markets for more than $137 billion in new debt, an historic surge in technology sector bond issuance. Morgan Stanley projects total hyperscaler borrowing will top $400 billion in 2026, more than double the $165 billion issued in 2025.

None of this means the AI buildout is wrong. It may be the most consequential infrastructure investment in the modern era. But it does mean the risk profile of cloud stocks has changed in a specific, measurable way. Most retail investors have not adjusted their position sizing to reflect it.

Here are the five warning signs worth watching.

Warning Sign 1: The Free Cash Flow Floor Is Already Gone

Free cash flow is what companies have left after capital expenditures. It is what funds dividends, buybacks, and debt repayment. It is also the most reliable input for any honest valuation of a technology stock.

For the last decade, the combined quarterly free cash flow of Amazon, Alphabet, Meta, and Microsoft averaged roughly $45 billion. It was one of the more extraordinary wealth-generating facts in corporate history. Four companies printing $45 billion every 90 days like clockwork.

Morgan Stanley projects that number will fall to approximately $4 billion in the third quarter of 2026. Their full-year free cash flow is on track to hit its lowest combined level since 2014, at a time when these companies’ revenues were about one-seventh of their current size.

Amazon is the most exposed. Morgan Stanley projects Amazon’s free cash flow will go negative by $17 billion in 2026. Bank of America’s estimate is a deficit of $28 billion. In an SEC filing earlier this year, Amazon disclosed it may seek to raise additional equity and debt as its buildout continues. The stock fell more than 8 percent the day after that earnings call. When a company that generated $38 billion in free cash flow in 2024 discloses it may go negative in 2026, the market is telling you something. The question is whether you are listening.

Warning Sign 2: How the Funding Model Shifted

The shift from cash-funded to debt-funded capex did not come with a press release. It accumulated across quarterly earnings calls from late 2024 forward, and most individual investors missed it.

Here is what it looks like in practice. Over just six months, Meta issued $55 billion in debt and paused its share repurchase program. Oracle’s 5-year credit default swaps, effectively the market’s insurance price against Oracle defaulting on its bonds, tripled from September 2025 to early 2026. UBS calculated that the acceleration in hyperscaler capex plans announced at Q4 earnings implies a $40 to $50 billion ramp in new borrowing, pushing total public market debt issuance from this sector to $230 to $240 billion this year alone.

“If you’re going to pour all this money into AI, it’s going to reduce your free cash flow,” said Jake Dollarhide, chief executive of Longbow Asset Management, in a February 2026 interview with CNBC. He was not wrong. The question is what that reduction means for stock prices in a sector that has been valued, until now, on its extraordinary cash generation.

Al Cattermole of Mirabaud Asset Management described the shift as breaking an “unspoken contract” with investors. Historically, owning cloud stocks meant owning cash-flow machines. Now it means owning companies running capex-to-revenue ratios of 25 to 30 percent, a range previously associated with capital-intensive utilities and telecommunications firms, not technology platforms.

To understand why the shift from cash-funded to debt-funded capital cycles changes the risk profile of the assets built on that debt, monetary analyst Lyn Alden’s book is an educational resource on how debt-financed infrastructure booms have historically resolved and what the signals look like before the resolution becomes obvious.

No products found.

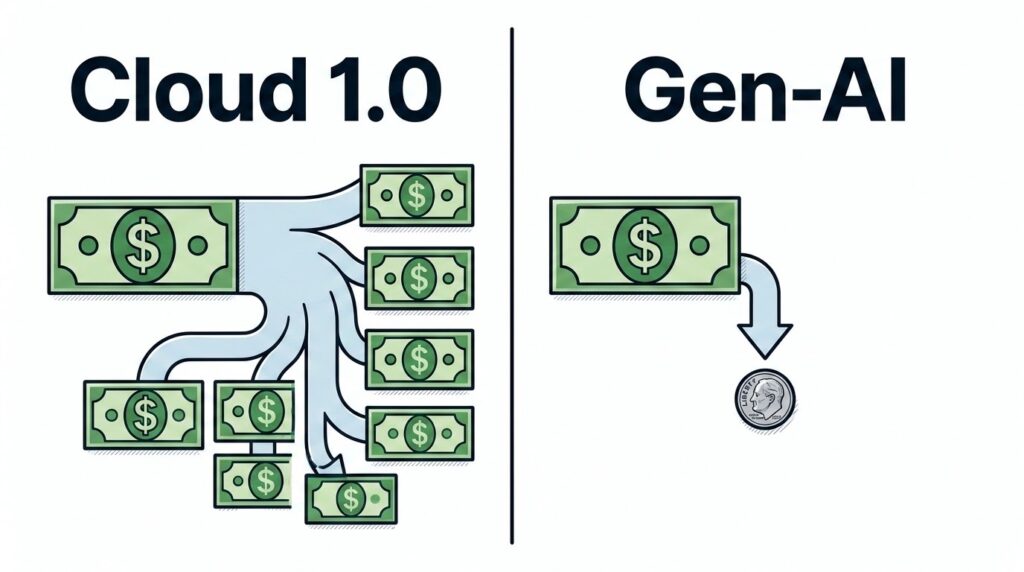

Warning Sign 3: The $0.20 Problem

This is the most important number in the article.

Rothschild’s Redburn research division downgraded both Amazon and Microsoft in November 2025. It was the first time analyst Alex Haissl had cut his ratings on either company since initiating coverage in June 2022. The downgrade was not about growth. It was about unit economics.

Redburn’s analysis found that Gen-AI infrastructure currently generates approximately $0.20 in net present value for every $1 spent. In the original cloud era, hyperscalers generated approximately $1.40 per dollar of capital deployed.

The reason for that gap is structural, not temporary. Cloud 1.0 featured cheap, standardized hardware; millions of enterprise customers with genuine switching costs; and strong pricing power that allowed margins to expand as the platforms scaled. Gen-AI inverts all three. The hardware is extraordinarily expensive and depreciates quickly as chip generations advance. The primary customers today are AI startups and enterprises still in early deployment, neither of which has the pricing sensitivity of an established cloud enterprise customer. And much of the economic value created by Gen-AI flows not to the cloud platforms hosting the models but to the model providers themselves.

“Gen-AI scales on a bloated, inefficient stack, while cloud 1.0 scaled only after achieving efficiency,” Haissl wrote in the downgrade note.

The bull case requires that the $0.20 figure improve materially as enterprise AI adoption scales. Google Cloud’s 63 percent year-over-year revenue growth in Q1 2026 is the clearest evidence that it can. The investor’s job is to determine whether the improvement is fast enough to justify current multiples while free cash flow is simultaneously collapsing.

Warning Sign 4: Morgan Stanley Put a Ceiling on the Good News

One of the more instructive moments of the 2026 earnings season came not from a bear but from Morgan Stanley. It is worth reading alongside Bank of America’s separate warning this week, which flagged seven bear market signposts triggered simultaneously. Two of the largest institutional voices on Wall Street are saying the same thing from different angles.

In a February 2026 note, Morgan Stanley wrote that the AI buildout had grown so large and so widely understood that it no longer justified paying any price for the companies driving it.

That framing deserves to sit with investors for a moment. This is not the view of a permabear. Morgan Stanley is one of the most consistently bullish institutional voices on large-cap technology. What the note was saying is that the market has moved from a phase in which AI infrastructure spending was a surprise catalyst to a phase in which it is fully priced into consensus expectations. In that environment, the risk is asymmetric: a revenue miss produces a large downside; a revenue beat produces a muted upside.

The same note added: “We don’t see this risk as a 2026 story, but vigilance is a 2026 responsibility.”

For investors, that framing is a conditional, not a comfort. The caution implied in that phrase requires active monitoring of specific quarterly metrics, not the passive assumption that because the AI buildout is real, the current valuation is justified. The broader question of whether AI stocks are structurally overvalued relative to the dot-com era is one we have examined separately. What the Morgan Stanley note addressed was something more immediate: the ceiling on upside from here.

Warning Sign 5: You Probably Own More of This Than You Think

The final warning sign is not about the companies. It is about your portfolio.

If you hold a broad S&P 500 index fund, you already have significant concentration in the five hyperscalers. The combined weight of Amazon, Alphabet, Meta, Microsoft, and Nvidia in the S&P 500 currently exceeds 25 percent of the index. A QQQ position is even more concentrated. The top five holdings represent roughly 40 percent of that fund. That is not an argument to sell either fund. It is an argument to understand what you own.

That concentration matters even more when a rotation out of mega-cap tech is already underway. Whether the current sector rotation has real staying power is a separate question from whether you are positioned for it. What is not debatable is that a 25 percent index concentration in five companies running the largest capital expenditure cycle in corporate history is a thesis position, whether you built it intentionally or not.

“Their full-year free cash flow is set to hit the lowest level since 2014, when their revenues were about a seventh of their current size,” analysts compiled by Visible Alpha noted in May 2026. That fact does not live in the typical index fund investor’s mental model of what they own. It should.

The Bull Case Is Not Wrong. But It’s Conditional

Every warning sign in this article has a counter-argument, and some of them are strong.

Google Cloud grew 63 percent year-over-year in Q1 2026, topping Wall Street estimates by nearly $2 billion. AWS posted its fastest growth rate in 15 quarters at 28 percent. Microsoft’s AI business now runs at an annualized revenue rate of $37 billion, up 123 percent year-over-year. The revenue is arriving. The backlog, contracted sales not yet recognized as revenue, across all five hyperscalers totals approximately $1.5 trillion.

The question is not whether AI revenue is real. It is whether the conversion rate from that backlog to recognized, high-margin, free-cash-flow-generating revenue is fast enough to justify deploying $725 billion in capital this year, much of it borrowed.

Morgan Stanley’s formula for the answer is specific: at AWS’s 13.1 percent operating margin and 28 percent revenue growth, the incremental return on invested capital on AI infrastructure exceeds 25 to 30 percent, the threshold that justifies the free cash flow drawdown during the build phase. If those numbers hold, the capex is demand-justified and the current multiples are defensible.

If they do not, if any of the major hyperscalers misses its AI revenue backlog conversion targets in Q2 or Q3 2026, the Redburn unit economics become the operative number. A re-rating of cloud positions toward cash-flow-based valuations, rather than revenue multiples, follows.

The verdict: the AI infrastructure spending boom is not a bubble in the traditional sense. It is a front-loaded capital cycle of historic scale, funded in part by debt, running on unit economics that have not yet closed the gap to cloud 1.0. The investments being made now will likely generate enormous returns over a decade. The question being asked in 2026 is whether the stocks already reflect that decade of value, and whether the path from here to there includes a meaningful correction in free cash flow that the current prices do not account for.

Hold if you have a 10-year horizon and own primarily through an index. Review your position sizing if you hold individual cloud names at multiples above 25 times forward earnings with free cash flow declining. In either case, the quarterly metrics below are the only numbers worth tracking.

The 3-Part Position Check

Run this before Q2 2026 earnings open.

First, calculate your actual hyperscaler concentration across all accounts. Add up your exposure to Amazon, Alphabet, Meta, Microsoft, and Nvidia, including what you hold through index funds. If the combined figure exceeds 25 percent of your investable assets, you have a concentrated thesis position, whether you intended to build one or not.

Second, apply the free cash flow test to any individual cloud stock you hold directly. If free cash flow yield, free cash flow divided by market capitalization, falls below 1.5 percent while the stock trades above 25 times forward earnings, the margin of safety has disappeared from that position.

Third, define your trigger before Q2 earnings. Write down the specific metric that would prompt you to reduce your position size. Candidates include: Amazon’s AWS operating margin falling below 11 percent, Google Cloud revenue growth decelerating below 40 percent year-over-year, or combined hyperscaler quarterly free cash flow staying below $10 billion in Q3. Defining the exit condition before the earnings report lands is the only way to avoid making a reactive decision after the market has already moved.

For educational purposes only. Not financial advice. Investing in equity securities involves risk, including the possible loss of principal. Past performance does not guarantee future results. Consult a licensed financial professional before making any investment decisions.

Frequently Asked Questions

Is AI infrastructure spending creating a bubble in cloud stocks? The most accurate description is a front-loaded capital cycle, not a classic bubble. Cloud stock valuations reflect genuine revenue growth: Google Cloud is up 63 percent year-over-year and Microsoft’s AI business runs at a $37 billion annualized rate. The risk is that current multiples already price in a decade of that growth, while free cash flow at the four largest hyperscalers is projected to hit its lowest combined level since 2014 during the peak spending years.

Which hyperscaler has the weakest return on its AI capex? Based on publicly available analysis, Microsoft and Amazon face the sharpest scrutiny. Redburn’s November 2025 downgrade of both companies cited Gen-AI unit economics producing roughly $0.20 in net present value per $1 spent, versus $1.40 per dollar in the cloud 1.0 era. Amazon’s situation is particularly acute: its 2026 free cash flow is projected to go negative by $17 to $28 billion, the first such deficit in its modern history as a cloud company.

Should I sell my cloud stocks if their free cash flow turns negative? Not automatically. Free cash flow turning negative during a capital buildout is a known feature of infrastructure investment cycles. Railroads, telecommunications, and the original internet buildout all went through extended negative free cash flow periods before generating substantial returns. The relevant question is whether the revenue conversion rate justifies the drawdown. For Amazon Web Services at 28 percent growth and 13 percent operating margins, the math is defensible. The metric to watch is whether operating margins hold as capex accelerates, not whether free cash flow goes negative in isolation.

What does the AI infrastructure spending boom mean for Nvidia and semiconductor stocks? Nvidia is structurally different from the hyperscalers in the current cycle. It is a primary beneficiary of the capex cycle rather than a company deploying capital at uncertain returns. Nvidia’s Q1 fiscal 2027 revenue grew 85 percent year-over-year. The risk for Nvidia is hyperscalers accelerating development of proprietary AI chips, which are expected to capture approximately 45 percent of the AI chip market by 2027, reducing Nvidia’s share of total AI chip spending.