The Dow Jones Industrial Average closed at 52,183 on Monday, up 307 points, or 0.59 percent, crossing 52,000 for the first time. The move capped a broader rally: the S&P 500 gained 1.18 percent, the Nasdaq rose 2.07 percent, and mega-cap tech names that had a rough week, including Alphabet, Amazon, Meta, and Tesla, bounced back as easing US-Iran tension and renewed talk of a tax-cut bill lifted sentiment broadly.

But the index milestone happened on the same day as a structural change that matters more than the round number. Alphabet officially replaced Verizon inside the Dow’s 30-stock lineup, a swap S&P Dow Jones Indices announced June 23 and executed before Monday’s open. Alphabet’s stock rose about 4 percent on its debut day. Verizon fell more than 5 percent, the index’s worst performer.

Most coverage of this event led with the round number. The number is the headline. The mechanism underneath it is what actually changes something for investors who hold Dow-tracking funds.

The Dow Doesn’t Work the Way Most Other Indexes Do

The S&P 500 and the Nasdaq weight their components by market capitalization. A trillion-dollar company moves the index more than a ten-billion-dollar company, because it represents a bigger share of the total market being measured. That’s intuitive. Bigger company, bigger influence.

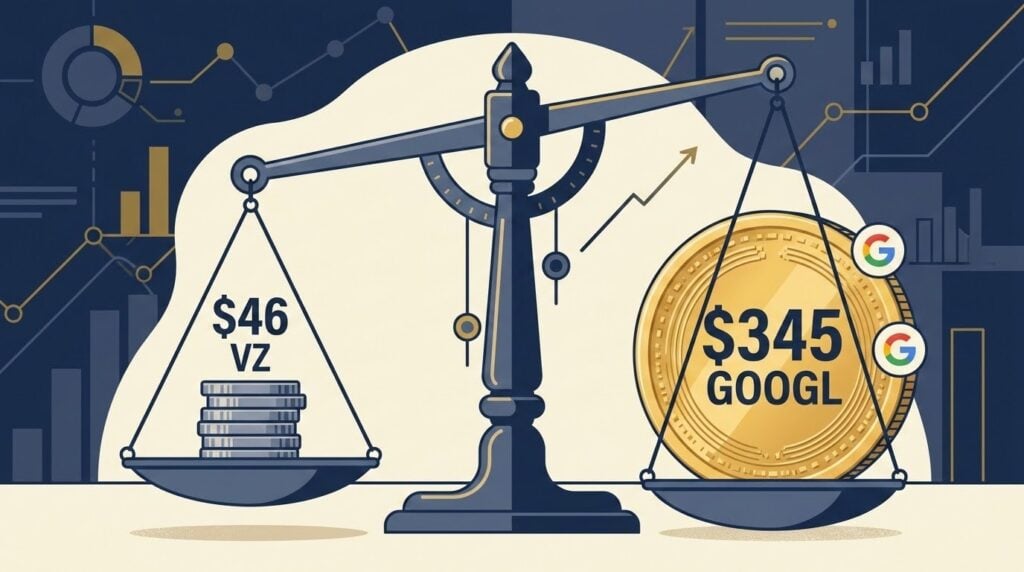

The Dow doesn’t do that. It’s price-weighted, a holdover from 1896 when the index was first calculated and the math was meant to be done by hand. The Dow adds up the share prices of all 30 components and divides by a single adjustable number called the Dow Divisor. A stock trading at $345 moves the index roughly seven times more than a stock trading at $46, regardless of which company is actually larger, more profitable, or more influential in the economy.

That’s exactly what happened here. Verizon, despite running the second-largest wireless network in the country and generating real free cash flow, had drifted down to about $45 a share. At that price, S&P Dow Jones Indices said Verizon accounted for only about half a percentage point of the entire index’s weighting, a level the index provider itself called immaterial. Alphabet, at roughly $345 a share, immediately became the Dow’s sixth most influential component the moment it joined.

Nothing about Verizon’s underlying business changed on June 29. It still serves more than 100 million wireless subscribers. It still pays a dividend yield north of 6 percent. What changed is that its low stock price had made it nearly invisible in an index that measures influence by price, not size.

What The Dow Jones Record High Actually Means If You Hold a Dow-Tracking Fund

If your retirement account or brokerage holds something tracking the Dow specifically, like the SPDR Dow Jones Industrial Average ETF, the fund had to mechanically sell its Verizon position and buy Alphabet before Monday’s open. That’s a real, forced transaction, not a metaphor.

The scale of that forced buying is smaller than it might sound. Assets specifically indexed to the Dow total around $115 billion. Assets indexed to the S&P 500, where Alphabet has been a member for years, total roughly $20 trillion. Alphabet was already owned by nearly every broad fund that would want to hold it. The Dow inclusion didn’t create new demand for Alphabet stock so much as it changed how much Alphabet’s daily price swings will now move your specific Dow-tracking fund relative to before.

The bigger structural fact: the Dow now holds five of the companies that dominate U.S. market capitalization, Apple, Microsoft, Nvidia, Amazon, and Alphabet. Combined with Salesforce, IBM, and Cisco, technology and communications names now make up roughly 22 percent of a 30-stock index built in 1896 to track agricultural, coal, oil, and steel companies.

A fund that tracks “the Dow” today carries more concentrated technology exposure meaningfully, and more sensitivity to AI spending cycles and interest-rate moves on growth stocks, than it did a decade ago. That’s not a defect. It’s a function of an index that periodically swaps in companies more representative of the current economy. But it does mean the word “Dow” describes a different basket of risk than it used to.

What The Dow Jones Record High Means If You Don’t Hold a Dow Fund

If your exposure runs through a broad market index fund, a target-date retirement fund, or anything tracking the S&P 500 or total market, almost nothing changed for you on Monday. Alphabet has been in those funds for years. The Dow’s internal reshuffling doesn’t touch your actual holdings.

That distinction matters because the Dow is the index most non-investors recognize by name, the number that gets quoted on the evening news, even though it represents a small, oddly-weighted slice of the market relative to broader benchmarks. A 307-point gain sounds large. As a percentage move, it was a 0.59 percent day, in line with the S&P 500’s 1.18 percent gain and well behind the Nasdaq’s 2.07 percent.

The Mechanics Are Either Noise or the Whole Point

There’s a real disagreement among serious investors about how much attention an event like this deserves.

- One school of thought holds that index mechanics like this are mostly noise. The point of owning a broad, low-cost index fund is to stop overthinking exactly which 30 or 500 or 3,000 stocks sit inside it on a given day and instead capture the market’s long-run return at minimal cost. Under that view, what matters is your fund’s expense ratio and turnover, not which name occupies which seat in a 130-year-old benchmark.

- The other school of thought says the mechanics are exactly the point. A structural quirk just handed a stock seven times more daily influence over a widely-watched index because of its dollar price, a number that has nothing to do with the size, quality, or fundamentals of the underlying business. Critics of passive investing’s growing dominance have argued for years that mechanical, rules-based index reshuffling can move real capital in and out of stocks for reasons that have nothing to do with whether those stocks deserve the money. This swap, on a smaller scale, is a clean example of exactly that critique in action.

This tension doesn’t resolve cleanly. While the case for ignoring index mechanics says a fund’s job is to capture the market, not interrogate its internal plumbing, field reality says that for the roughly $115 billion specifically benchmarked to the Dow, Monday’s swap was a real, mechanical reallocation driven entirely by share price.

This distinction works until your fund is the one being rebalanced. For anyone holding the S&P 500 or a total market fund, this is genuinely irrelevant. For anyone holding a Dow-specific product, it just changed what’s actually inside the basket and how it will behave the next time mega-cap tech has a rough week.

Mark Malek, chief investment officer at Siebert Financial, called Alphabet’s addition a “blue-chip endorsement” of the company’s AI investment, a framing that treats the inclusion as validation. Others in the market noted a more mechanical read: Alphabet was already in every major index that matters by assets under management, and the practical effect of Monday’s change was modest and contained almost entirely to Dow-specific products.

Both readings are defensible. Neither one tells you whether Alphabet is a good investment at its current price, a separate question entirely that depends on the company’s cloud revenue growth, search revenue growth, and the roughly $180 to $190 billion in AI infrastructure spending it has guided for this year, numbers that will matter to Alphabet’s stock price long after this index swap is forgotten.

The story of how indexing went from a fringe academic idea to a $20 trillion force in modern markets, including the quirks and tradeoffs built into benchmarks like the Dow, is well documented in Trillions by Financial Times journalist Robin Wigglesworth, one of our informational picks for understanding how the funds in your 401k actually work.

FTC disclosure (adjacent, per brand filter): TheCapitalist.com participates in the Amazon Associates program. We may earn a commission on qualifying purchases made through the link above, at no additional cost to you. This does not influence our editorial coverage.

The Takeaway

The number that made headlines, 52,000, is a round milestone with no inherent meaning. The mechanism underneath it, a 130-year-old index that still weights its 30 components by dollar price rather than company size, is the part actually worth understanding, because it determines what you own if you hold a Dow-tracking fund and how sensitive that fund now is to a handful of expensive technology stocks.

For educational purposes only. Not financial advice.

Frequently Asked Questions:

Is the Dow Jones Industrial Average the best way to measure the stock market?

No single index captures the whole market, but the Dow is generally considered less representative than the S&P 500 or a total market index. It includes only 30 companies, and because it’s price-weighted rather than weighted by company size, a handful of high-priced stocks can move it disproportionately. Most professional investors use the S&P 500 as their primary benchmark.

Why didn’t Verizon’s removal from the DJIA hurt its actual business?

Index inclusion and exclusion are about a benchmark’s composition, not a company’s operations. Verizon still runs its wireless network, serves its customers, and pays its dividend the same way it did before June 29. Being dropped from the Dow reflects a low stock price relative to other Dow components, not a verdict on the underlying business.

Does joining the Dow force a stock’s price higher?

Only modestly, and mostly in the short term. Funds that specifically track the Dow have to buy the new component and sell the old one, but the total assets benchmarked to the Dow are a small fraction of what’s benchmarked to broader indexes like the S&P 500. For a stock like Alphabet that was already widely held, the forced-buying effect is limited.

What should I actually check if I hold a Dow-tracking fund?

Confirm whether your fund or ETF tracks the Dow specifically (like DIA) versus a broader index like the S&P 500 or a total market fund. If it’s Dow-specific, understand that your fund now carries more concentrated exposure to mega-cap technology stocks than it did before this swap, which changes how it may behave during tech-sector volatility.