QUICK SUMMARY: The Strait of Hormuz closed again over the weekend after Iran reversed Friday’s reopening. As a result, stock futures are down, oil is up, and the VIX popped before breakfast. As long as Hormuz remains closed, the portfolio question should not be whether to sell but rather whether you have a pre-built rule for weekends like this one. Here is what the closure means and the move to make before 9:30 a.m.

The weekend rewrote Friday’s story in 48 hours. On Friday, Iran’s foreign minister declared the Strait of Hormuz completely open to commercial traffic, oil dropped almost 10%, and the S&P 500 closed at a record 7,126. On Saturday, the Islamic Revolutionary Guard Corps reversed the declaration and said the Strait of Hormuz was closed again to all vessels. On Sunday, the U.S. Navy seized an Iranian-flagged cargo ship attempting to run a blockade. By Monday’s pre-market open, S&P futures were down 0.6%, oil was up nearly 7%, and the VIX had jumped above 19 for the first time in two weeks.

If this is the first email you are reading this morning, the instinct is to ask what the closure means and whether to sell. That is the wrong question. The right question is the one almost no one is asking.

The Strait of Hormuz closed again. The pattern is the story, not the closure

This is not the first reversal. It is the third in six weeks. Ceasefire headlines, blockade announcements, peace talk collapses, sudden openings, sudden closings. Each one moves the market several percent in one direction. Each one is followed, a few days later, by the opposite move. The retail investor who reacts to each one is paying a tax every round-trip, in spreads, in short-term capital gains, and in the time between the sell and the buy-back when the market moves against them.

Interactive Brokers’ chief strategist Steve Sosnick put the psychology plainly this week: “At this point, it’s almost a feeding frenzy. No one wants to be left out. FOMO is a weird thing, because you know that the F is clearly ‘fear,’ but it’s really ‘greed.'”

That is the real engine of the last six weeks. It is not oil. It is not the Strait of Hormuz. It is investors jumping in on the rally days and jumping out on the reversal days and calling it a strategy.

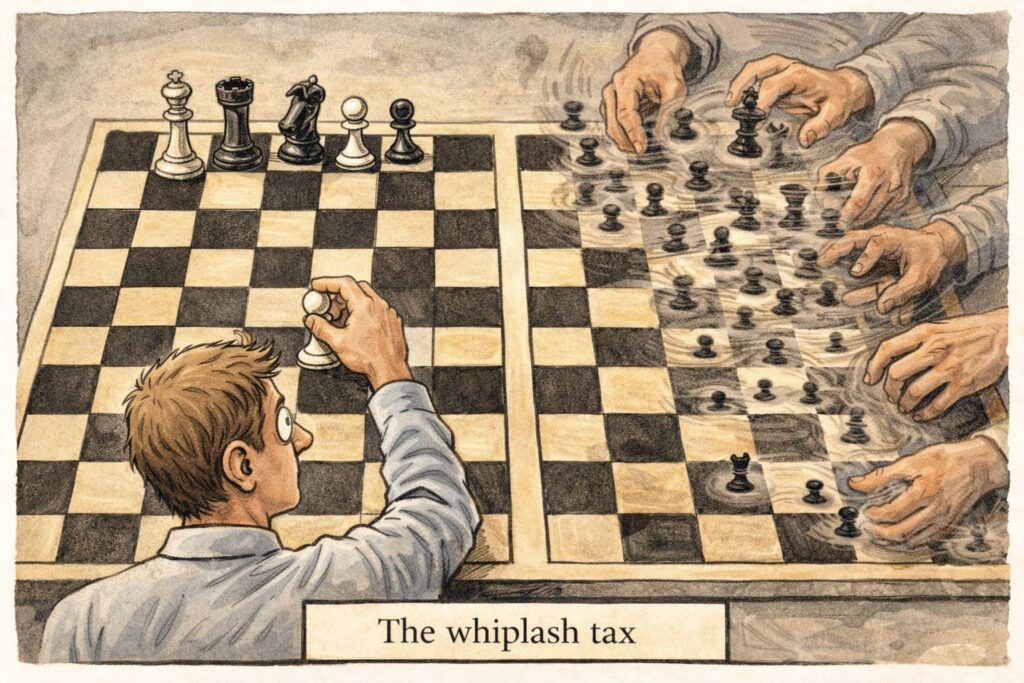

What the whiplash tax actually costs

The whiplash tax is the sum of what you lose each time you react to a reversible headline. It shows up in four places. The bid-ask spread you cross every time you sell and buy back. The short-term capital gains rate on any position held less than a year can run 10 to 20 percentage points higher than the long-term rate. The timing error, where the market moves against you between the sell and the re-entry. And the behavioral drift, where each round-trip lowers the threshold for the next one. In this case, the Strait of Hormuz closed, then opened, then closed again in quick succession. In total, there were 3 reversals in 6 weeks. Every time, the market reacted wildly.

Put concrete numbers on it. An investor with a $500,000 portfolio who round-trips 30% of their position during a single ceasefire-reversal cycle pays roughly $150 in spread cost, potentially $3,000 to $6,000 in short-term tax drag on gains that would otherwise compound, and anywhere from 1% to 4% in timing-error slippage if the re-entry happens on a rally day rather than a reversal day. Across three reversals in six weeks, the same investor is looking at a 3% to 8% drag on the traded portion of the portfolio. That is the whiplash tax. It does not show up on a statement with a line item. Instead, it shows up as the gap between what the account could have been and what it is.

Vanguard’s longer-run data on cash-holding behavior puts the durable cost in sharper relief. Investors who moved to cash for three months between 1980 and 2024 underperformed a 60/40 portfolio by an average of 4.1%. Six months in cash, 7.4%. Twelve months, 13.3%. In short, the whiplash tax is a short-dated version of the same mechanism.

The Strait of Hormuz closed, opened, then closed again.

The macro sequence is worth knowing, even if it does not require a trade. Oil is an inflation input, not a panic signal. The transmission runs in a specific order: oil price, CPI print, Federal Reserve path, bond yields, real rates, equity multiples. A single Monday spike in crude does not move that chain. A sustained price does.

The threshold worth watching is roughly $95 per barrel, sustained for three consecutive weeks. Below that, or below that duration, the Fed’s April 28-29 meeting can still hold to its current path. Chicago Fed President Austan Goolsbee has already signaled that an energy-driven inflation impulse could push the first rate cut into 2027. That is the regime question. If this was not answered this morning, it will not be answered this week.

For the long-horizon investor, the distinction matters in one direction only. A weekend reversal is noise. A two-month trend is a regime. The time to act on the regime is when the data clears the threshold, not when the headline hits the inbox.

The smart move to make now that the Strait of Hormuz closed yet again

The honest answer for most readers is that no trade belongs in the next hour, unless you don’t fear the whiplash tax. The investor actions worth taking this morning are structural, not reactive.

- Do not sell into the open. Gap-down selling realizes the round-trip cost this piece is warning against. If the current allocation cannot be held through a 50% drawdown without selling, the allocation was wrong before the weekend. This morning is evidence, not cause.

- Check whether the short-term cash bucket is funded. For investors within five years of retirement, the next 12 to 24 months of expenses should already sit in cash or short Treasuries, not in equities at all-time highs. If that bucket is underfunded, the Monday morning action is a bond-to-cash reallocation, not an equity sale. The difference matters. Bonds sold into strength pay the tax of growth; equities sold into weakness pay the tax of timing.

- Leave automatic contributions alone. Systematic buying through whiplash is the mechanism that produces retirement outcomes. Today is exactly the day the systematic investor stops thinking and keeps buying. An investor who pauses the 401(k) contribution this morning and resumes in July will have bought at materially higher prices for the months in between.

- If concentrated equity exposure is material, this is the week to write the exit criteria. A single stock, an employer stock position, or a sector ETF that represents more than 20% of the portfolio is a structural risk regardless of the headline cycle. The time to define the sell trigger is a quiet week, not a red Monday. Write the criteria now. Execute later, if ever.

- Do nothing else until the Federal Reserve meets on April 28-29. A closed strait on a Monday is not a Fed regime change. A closed strait two weeks from now with oil sustained above $95 might be. Wait for data that crosses the threshold before doing anything other than the four actions above.

What this piece is not saying

No analysis above knows whether the closure holds. Today, the Strait of Hormuz closed. Tomorrow and the day after? Not so sure. No one knows whether oil reverts, whether the ceasefire resumes, whether the Fed cuts in June or December, or even at all. The piece is not a forecast. It is a decision framework.

The investors best positioned on Wednesday are the ones who already knew, before the weekend, what Monday required of them. Their rule was written in a calm week and survives a loud one. Readers who find themselves scrambling to decide this morning have learned the most valuable thing a volatile market teaches: the rule has to exist before the weekend arrives, not during it.

Nick Maggiulli’s Just Keep Buying lays out the data case for why automatic contributions beat market-timing decisions across virtually every historical period, and is a useful educational partner for readers building the contribution discipline this article assumes. For readers focused on why market whiplash feels new every time, yet never is, Morgan Housel’s Same as Ever is an informative companion to the patterns that repeat.

Welcome to The Dire Straits

With the Strait of Hormuz closed again this morning, the investor question is not what happens next. Nobody knows. The question is whether the plan holds through the morning without modification. If it does, the plan is working. If it doesn’t, this is not the weekend to build a new one in 30 minutes. This is the weekend to learn that the next plan has to exist before the next closure, which is probably already being negotiated somewhere over a conference table that the market has not yet seen. At any rate, fear the whiplash tax.

Frequently Asked Questions

Should I sell stocks this morning because the Strait of Hormuz closed again?

No. Selling into a weekend gap-down usually realizes the round-trip cost of whiplash trading, meaning the investor sells low on Monday and often buys back higher later in the week when the closure reverses. If the current allocation cannot be held through this kind of volatility without selling, the allocation was too aggressive before the weekend. That is the lesson, not the headline.

What happens to oil and gas prices if the closure holds?

WTI and Brent crude jumped nearly 7% on Monday futures, putting both benchmarks back in the mid-$80s to mid-$90s range. If the closure sustains more than two to three weeks, retail gasoline prices would likely follow within 30 to 45 days. The transmission to the broader inflation print is slower and depends on strategic petroleum reserve draws and alternative supply routes.

With the Strait of Hormuz closed again, will the Federal Reserve delay rate cuts?

It can. Fed officials have already signaled a wait-and-see posture heading into the April 28-29 meeting. Sustained oil prices above $95 per barrel for several weeks would show up in the May and June CPI prints, which will likely push the first rate cut into late 2026 or into 2027. The operative word is sustained. A single Monday spike does not move the Fed. A two-month trend does.

Should I hold more gold or energy stocks during geopolitical volatility?

This is an allocation question, not a today question. Investors with heavy domestic equity concentration benefit from diversification into commodities, gold, and international equity, but that benefit compounds over quarters and years, not over a single morning. Building the diversification during a price spike pays the spike premium. Build it in quiet markets and hold it through loud ones.