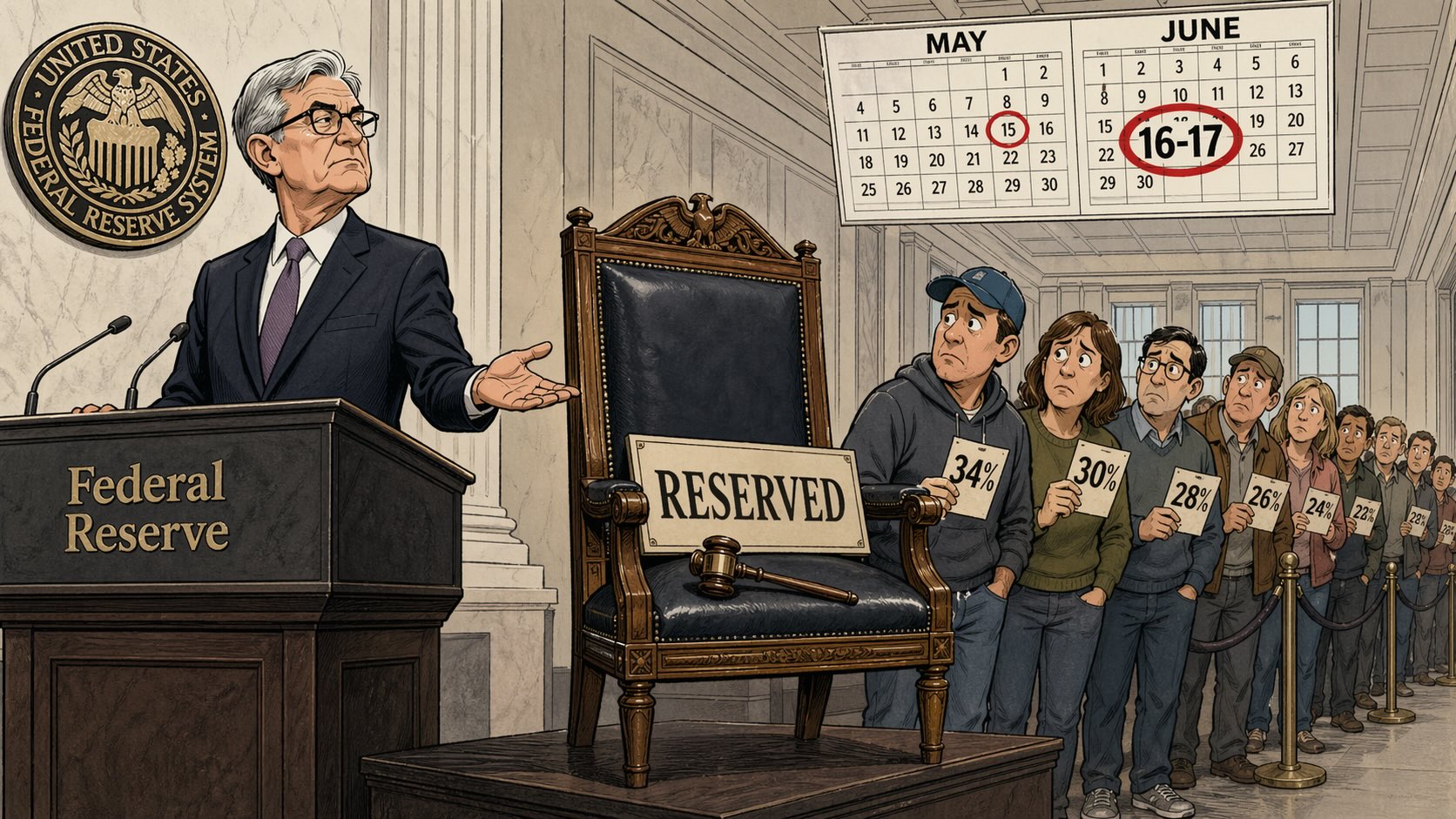

QUICK SUMMARY: Kevin Warsh faced the Senate Banking Committee on April 21, 2026, for his Federal Reserve chair confirmation hearing. Prediction markets are pricing only 30 to 34 percent odds of confirmation by May 15, when Jerome Powell’s term expires. The real investor question is not whether Warsh gets confirmed. It is whether the allocation you hold today can survive all three succession scenarios without forcing a sale.

Yesterday, Kevin Warsh appeared before the Senate Banking Committee and brought his credentials. He served on the Federal Reserve Board of Governors from 2006 to 2011 and held senior economic policy roles under the Bush administration. He also spent the last decade as a visiting fellow at the Hoover Institution. However, his confirmation as Federal Reserve chair won’t be moving on that basis.

Senator Thom Tillis, a senior Republican on the committee, vowed to vote against advancing the nomination until the Department of Justice drops its criminal investigation into Powell. The committee sits 13 Republicans to 11 Democrats. A single Republican defection deadlocks the vote. Tillis has called Warsh’s qualifications “impeccable” and said he wishes he could vote yes. He will not do so until the Powell investigation ends.

Prediction markets absorbed the developments quickly. Polymarket puts the odds of confirmation by May 15 at 34 percent while Kalshi sits at 30 percent. Both show odds rising to 73 to 85 percent by July, which tells you the market expects resolution, but not on the original schedule.

That gap matters. Powell has publicly committed to staying on as chair pro tempore until Congress confirms his successor. He also said he will not leave the Board of Governors, where his term runs to January 2028, until the DOJ investigation ends. President Trump has threatened to fire him if he tries. A federal judge has already blasted the DOJ investigation as an unjustified act of intimidation. If Trump attempts the firing, Powell is widely expected to sue.

The base case the market is pricing is not “Warsh replaces Powell on May 15.” It is “Powell stays as chair pro tempore through a contested transition into summer, with a legal challenge possibly active in parallel.”

Regime Change Means More Than a New Name on the Door

At the hearing, Warsh used specific language that most investors missed. He said he wants “regime change” at the Federal Reserve. That is not standard confirmation-hearing theater. It is a direct statement about the institution.

Three doctrinal positions came through clearly. First, he wants to reduce the Fed’s balance sheet, which currently sits at $6.7 trillion. He has argued for years that the post-2008 asset purchase programs left the Fed too deeply entrenched in the economy and that the balance sheet should have been unwound long ago. Second, he is skeptical of forward guidance, the practice of signaling where the Fed wants rates to go before it moves them. He would abandon it. Forward guidance is how bond markets have been pricing the rate path for over a decade. Third, he dismissed the Fed’s preferred inflation measure, the core personal consumption expenditure index, as “a rough swag.” He wants a different measurement framework.

These are not rate-decision questions. They are monetary regime questions. A new chair who maintains the post-2008 doctrine is a cosmetic change. A new chair who rewrites it, as the nominee has openly signaled, is a structural one. The confirmation fight is about the name on the door. The regime question is about what happens to the rate path, the dollar, and the long end of the Treasury curve for the next four years.

Inflation is currently running at 3.3 percent, above the Fed’s 2 percent target. The Iran war and the resulting gasoline spikes have made that number harder to pull down, not easier. A chair who wants to cut into a 3.3 percent environment has to explain why, and Warsh has a long public record criticizing Powell for failing to tighten pre-emptively in 2021. The likeliest scenario is not a rapid cut. It is a slower rate path with faster balance sheet reduction, less forward guidance, and a changed inflation framework. That is a meaningfully different environment for bonds than the consensus has been pricing.

The Decision Framework for the Next Eight Weeks

One reader email captured the trap bluntly: “I went to cash because I was positive Trump would do something to crash the market. That turned into a true not-to-brag because now markets have completely recovered and I don’t know what to do.”

That investor is about to get another chance to repeat the mistake. The Warsh succession will produce at least four or five more market-moving headlines between now and June, much like the weekend headline whiplash that marked the Strait of Hormuz closures. The DOJ will respond or not. Tillis will hold or fold. Powell will stay or leave. Trump may attempt a firing. Each headline will move the market several percent in one direction. Each will be followed, a few days later, by the opposite move.

The discipline that separates investors who compound through this from investors who pay a headline tax on every round-trip is simple, and almost no one runs it. Write down the three scenarios and assign each a probability.

- Scenario 1: Clean confirmation by May 15. Requires the DOJ to drop the Powell investigation. Current market-implied probability: roughly 30 to 34 percent.

- Scenario 2: Delayed confirmation into July, with Powell as chair pro tempore in the interim. Requires Tillis to relent after recess or the investigation to resolve. Market-implied probability: roughly 40 to 50 percent.

- Scenario 3: Contested transition with a Trump-initiated Powell firing and lawsuit. Lowest probability, highest market impact. Roughly 15 to 25 percent.

For each scenario, write down what happens to your position, what you would do about it, and the single piece of public news that would confirm the scenario is active. If you cannot do all three, you do not understand the trade well enough to make it. Hold what you have.

Annie Duke’s Thinking in Bets lays out this probabilistic decision framework in detail, and is a useful educational partner for readers building the scenario-planning discipline this article assumes.

As such, the real deadline isn’t May 15. It becomes June 16-17, which is the next FOMC meeting after Powell’s chair term ends. That is where an interim-chair question becomes a live policy question. Build your plans backward from that date.

The Portfolio Move

The allocation that survives all three scenarios without forcing a sale is the right one. If the portfolio is already positioned for four macro environments, growth up, growth down, inflation up, and inflation down, the confirmation outcome does not require a trade. If it is not, the next eight weeks are the rebalancing window. Reduce concentration in long-duration Treasuries. Add gold to the upper end of strategic weight. Keep international equity exposure. Do not chase rate-cut bets in anticipation of a dovish incoming chair. Inflation at 3.3 percent constrains any chair.

For active traders, the confirmation calendar is a set of dated catalysts. Tillis’s position is the binary trigger. Watch short-duration Treasury yields for the cleanest signal on confirmation odds, the dollar index for the cross-asset read, and gold as the hedge against a disorderly transition. Long-duration Treasuries are the crowded trade. If Warsh confirms and signals faster balance sheet reduction, the long end sells off before the short end moves.

The one move that fits every reader: if you are tempted to trade on the next headline, write down what change you would make, what would trigger it, and what you would do if the headline reversed within 48 hours. If you cannot answer all three, the trade is not ready to execute.

Morgan Housel’s Same as Ever addresses the behavioral patterns that repeat through every Fed transition, and is an informative companion to the discipline of holding through headline noise.

The Rule Worth Owning

Kevin Warsh’s confirmation is not one event. It is a series of headlines spread across eight to twelve weeks, any of which can move the market three to five percent in either direction. The investor who writes the exit triggers before the catalyst fires compounds. The investor who waits to decide until the headline hits pays a tax on every round-trip. The regime question outranks the rate question. The June FOMC outranks the May 15 deadline. And the allocation that can survive all three scenarios without forcing a sale is the one that does not need to be traded at all.

Frequently Asked Questions

Will Kevin Warsh be confirmed as Fed chair by May 15?

Prediction markets currently price the odds at 30 to 34 percent. The block is not ideological. Senator Thom Tillis has said he will not vote to advance the nomination until the Department of Justice drops its criminal investigation into Powell. Without Tillis, the Senate Banking Committee deadlocks 12-12 and the nomination fails. Odds rise to 73 to 85 percent by July on the assumption the investigation resolves in the interim.

What Happens to the Fed on May 15 if the Nomination Remains Blocked?

Current Fed Chair Jerome Powell said he will remain as chair pro tempore until his successor is confirmed. His term as a member of the Board of Governors runs to January 2028, so he has legal standing to stay on the board even after his chair term ends. President Trump has threatened to fire him if he does, which would likely trigger a lawsuit.

Would a Warsh-led Federal Reserve Cut Interest Rates Faster?

Not necessarily. The nominee has a long public record criticizing Powell for being too slow to tighten in 2021 and too accommodative afterward. Inflation is currently running at 3.3 percent, above the Fed’s 2 percent target, which constrains any chair. He is more likely to move faster on balance sheet reduction and change the inflation measurement framework than to cut rates aggressively into elevated inflation.

How Should This Affect My Retirement Portfolio?

The allocation question is largely independent of the confirmation outcome for investors with 10 or more years to retirement. For pre-retirement readers, the relevant issue is sequence-of-returns risk, not the Fed chair succession. If the next 12 to 24 months of expenses are not already in cash or short Treasuries, fund that bucket from bonds sold into current strength. Do not rebalance the equity bucket based on the confirmation calendar.