Mega-cap technology stocks are not entering the next earnings cycle as underdogs. They are entering it as market leaders with very little room for disappointment.

That is the problem.

The companies at the center of the artificial intelligence trade remain dominant businesses. Microsoft, Nvidia, Apple, Amazon, Alphabet, Meta, and Tesla still shape the market’s earnings, capital spending, and investor psychology. But the question has changed. Wall Street is no longer asking whether these companies have a credible AI story. It is asking whether that story is producing enough return to justify the prices investors are already paying.

For retirement-minded investors, that distinction matters. A 35-year-old adding to an index fund every month can treat a rough tech earnings season as background noise. A 62-year-old with 40% of a retirement portfolio tied to five mega-cap technology names is facing a different kind of risk. The danger is not that AI fails overnight. The danger is that your portfolio may already be priced for AI success with no margin for error.

Magnificent Seven Earnings Risk Is No Longer Just About Revenue Growth

For the past three years, investors rewarded AI ambition. More chips. More data centers. More cloud capacity. More capital spending. More promises about copilots, agents, automation, and enterprise productivity.

That phase made sense early in the cycle. Markets often reward the companies that appear best positioned to own the next major platform shift. But as the AI trade matures, investors are moving from possibility to proof. That means earnings reports are being judged differently.

A company can still beat revenue expectations and watch its stock fall if guidance does not support the valuation. That is what makes this earnings cycle more difficult for investors who have grown used to mega-cap tech leading almost automatically.

Microsoft is a useful example. In its official FY2026 Q2 release, Microsoft reported $81.3 billion in quarterly revenue, up 17% year over year, with Azure and other cloud services revenue up 39%. Those are not weak numbers. Yet Charles Schwab’s post-earnings analysis, “Less Magnificent: Why Mega-Caps Limp Post-Results,” noted that several mega-cap tech names sold off after earnings as investors questioned guidance, valuation, AI spending, and the law of large numbers.

That is the new bar.

A revenue beat is not a clear thesis. A strong cloud number is not automatically enough. A bigger AI budget is not automatically bullish.

The market wants evidence that spending is turning into durable earnings power.

The Earnings Deceleration Is Already Showing Up Under the Surface

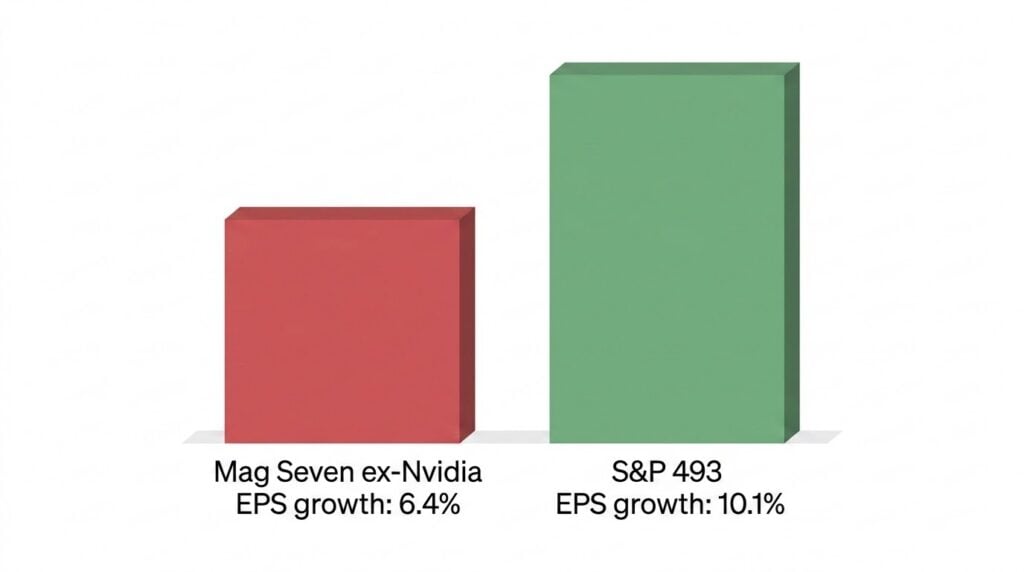

The headline Magnificent Seven earnings number still looks strong. The underlying number looks less comfortable. According to FactSet’s April 2026 analysis, “Excluding NVIDIA, ‘Mag 7’ Companies Expected to Report Lower Earnings Growth Than Other 493,” the Magnificent Seven were expected to report 22.8% year-over-year earnings growth for Q1 2026.

That sounds impressive.

But FactSet also found that if Nvidia were excluded, the group’s expected earnings growth fell to 6.4%. The remaining 493 companies in the S&P 500 were expected to grow earnings at 10.1%.

That is the core of the problem. Remove Nvidia from the Magnificent Seven and what remains is growing earnings slower than the rest of the market. This does not mean the other mega-cap tech companies are broken. It means the market’s leadership has narrowed. It also means investors who believe they own a broad AI growth basket may actually be relying heavily on one earnings engine.

FactSet’s full-year 2026 estimates showed the same issue. The Magnificent Seven were expected to grow earnings by 24.6% for calendar 2026. But excluding Nvidia, that number fell to 13.2%, below the 15.9% expected earnings growth rate for the other 493 companies.

This is not a crash forecast.

It is a concentration warning.

If a small group of stocks gets premium valuations, that group has to keep producing premium growth. If the growth advantage narrows, the valuation advantage becomes harder to defend.

Why Good Earnings Can Still Produce Bad Stock Reactions

Investors often assume that if a company beats earnings, the stock should rise. That is not how expensive stocks work.

At 30 times forward earnings, investors are not paying for one good quarter. They are paying for years of strong revenue growth, expanding margins, disciplined capital spending, and management guidance that supports the entire valuation. That leaves little room for ordinary disappointment.

A mega-cap tech company can report record revenue, raise capital spending, talk confidently about AI demand, and still face selling pressure if investors do not see enough near-term return on that spending. This is where many retirement investors get caught. They look at the company and say, “This is a great business.”

They may be right.

But the better question is, “Is this great business still a good holding at this size, at this price, in this stage of my retirement plan?” Those are different questions.

Microsoft can be a great company and still be too large a position for a retiree who needs portfolio stability. Nvidia can remain central to the AI buildout and still carry valuation risk. Apple can generate enormous cash flow and still move sideways if growth slows. Amazon can dominate cloud and commerce and still disappoint if margins do not meet expectations.

Great companies do not eliminate portfolio risk. Sometimes they create a different version of it: confidence risk. That is the risk that investors become so comfortable owning the winners that they stop measuring how much of their financial future depends on those winners continuing to win.

The Concentrated Portfolio Problem Most Investors Have Not Named

Many investors believe they are diversified because they own the S&P 500.

That is only partly true.

A recent Visual Capitalist breakdown, “Every S&P 500 Company in One Giant Chart,” reported that the top 10 companies made up more than 36% of the S&P 500 as of March 30, 2026. Nvidia alone had a 7.0% index weight, Apple had 6.3%, and Microsoft had 4.6%. That means a broad market index fund is less broad than many investors assume.

Now add a Nasdaq fund, a growth ETF, or individual positions in Nvidia, Microsoft, Apple, Amazon, Alphabet, Meta, or Tesla. Suddenly, a portfolio that looks diversified on paper may be heavily dependent on one market theme: mega-cap technology driven by AI expectations.

This is how accidental concentration happens.

Nobody sets out to make their retirement depend on one trade. But after several years of outperformance, portfolio drift can do it for you.

Consider a $900,000 retirement portfolio with 45% in mega-cap technology. That is $405,000 tied to one dominant market theme. If that sleeve falls 25%, the portfolio takes a $101,250 hit before accounting for any spillover into the rest of the market.

That may be survivable.

But it should not be surprising. The test is simple: if your largest technology position fell 30% after earnings guidance, would you still hold it? If the honest answer is no, the position is probably already too large. Not because the company is bad. Not because AI is fake. Not because a crash is guaranteed. Because your real risk tolerance is lower than your stated risk tolerance.

The Retirement Risk Is Different From the Accumulation Risk

The same portfolio can be reasonable for one investor and reckless for another.

A 40-year-old with a stable income, no planned withdrawals, and a 20-year time horizon can hold through a sharp tech drawdown. In fact, if that investor is contributing regularly, lower prices may help long-term returns.

A 67-year-old drawing income from the portfolio does not have the same setup.

That investor faces sequence-of-returns risk. A portfolio decline early in retirement can do more damage than the same decline during the accumulation years because withdrawals force shares to be sold when prices are down. That is why earnings season matters more for retirees than it does for younger investors. The issue is not whether to predict the next stock move. The issue is whether the portfolio can absorb a guidance-driven selloff without forcing bad decisions.

A retiree who has 12 to 24 months of withdrawals funded through cash, Treasury bills, short-term bonds, or other conservative reserves may be able to ride out volatility. A retiree who needs to sell appreciated mega-cap tech shares every month to fund living expenses has less flexibility.

That difference matters. The first investor has a plan. The second investor has a price dependency.

The Case for Staying Invested Is Still Strong

There is an important counterargument here: most investors damage their returns by doing too much.

That argument deserves respect.

Quarterly earnings are noisy. Guidance can be conservative. Analysts can overreact. Stocks can fall after good numbers and recover weeks later. Investors who repeatedly trimmed mega-cap tech in 2023, 2024, and 2025 because valuations looked stretched paid a real opportunity cost. The AI trade compounded far beyond what many traditional valuation models suggested. That is why this is not a blanket argument to sell technology stocks.

For long-term investors with diversified portfolios, the best move may still be to contribute on schedule, rebalance periodically, and ignore earnings volatility. For investors who want the classic long-run case for staying invested instead of trying to outguess every market turn, Burton Malkiel’s A Random Walk Down Wall Street remains one of the clearest arguments for why market timing is so difficult.

The point is not that every investor should trim mega-cap tech before earnings.

The point is that staying invested does not require staying overconcentrated.

A fully invested bear is still a bull in the only way that matters: they stayed in the market.

But a retiree with 45% of a portfolio in five mega-cap names is not simply “staying invested.” That investor is running a concentrated position at a stage of life when recovery time matters.

That is a different decision.

What Investors Should Do Before the Next Tech Magnificent Seven Earnings Cycle

The first step is not to sell. The first step is to measure.

Add up your exposure to mega-cap technology across every account. Include S&P 500 index funds, Nasdaq funds, growth ETFs, sector ETFs, individual stocks, and company stock from current or former employers.

Most investors underestimate this number. Once you know the number, run a drawdown test. If your mega-cap tech exposure fell 25%, what would happen to your total portfolio? Would you still have enough cash or fixed income to fund withdrawals? Would you rebalance into the decline? Would you freeze? Would you sell after the drop? Write the answer down before earnings.

If you cannot write a calm plan today, you probably will not make a better decision during a selloff. For investors more than 10 years from retirement, the answer may be simple: keep contributing, rebalance on schedule, and do not treat every earnings report as a trading signal.

For investors within five years of retirement, the answer should be more deliberate. If mega-cap tech is more than 35% to 40% of your portfolio, consider trimming back to a target allocation before volatility forces the decision.

For investors already retired, the focus should be withdrawal safety. Fund near-term income needs from conservative assets so you are not forced to sell equities into a drawdown.

There is also a broader market rotation developing under the surface. Our recent analysis on small-cap stocks outperforming mega-cap tech explains why some investors are starting to look beyond the handful of names that led the last bull market.

That does not mean abandoning the winners.

It means asking whether the winners still deserve the same weight in your portfolio that the market gave them after years of outperformance.

Magnificent Seven Earnings Risk Comes Down to One Question

The question is not whether AI is real.

It is.

The question is not whether the largest technology companies are important.

They are.

The question is whether your portfolio is priced as if nothing can go wrong.

That is where investors need to be honest.

A company can dominate its industry and still disappoint its shareholders. A stock can fall even after a revenue beat. A market-cap-weighted index can create more concentration than investors realize. A retirement portfolio can look diversified while depending too heavily on one earnings theme.

The next tech earnings cycle will not settle the AI debate.

But it may reveal which investors own AI exposure as part of a plan and which investors simply drifted into concentration because the trade worked.

If your plan still works after a 25% drawdown in your largest tech positions, stay disciplined. If it does not, reduce the risk before the market decides for you.

For educational purposes only. Not financial advice.

Frequently Asked Questions

What is the biggest Magnificent Seven earnings risk right now?

The biggest risk is that valuations already reflect strong AI-driven growth. If guidance does not show that AI spending is turning into durable earnings, margins, and cash flow, mega-cap tech stocks can fall even if the companies report solid headline numbers.

Does the FactSet data mean the Magnificent Seven are in trouble?

Not necessarily. FactSet’s Q1 2026 data shows that Magnificent Seven earnings growth is still strong as a group. The warning is that Nvidia is carrying a large portion of that growth. Excluding Nvidia, expected earnings growth for the remaining Magnificent Seven falls below the earnings growth rate of the other 493 S&P 500 companies.

Are S&P 500 index fund investors too concentrated in mega-cap tech?

Some may be more concentrated than they realize. Visual Capitalist reported that the top 10 companies made up more than 36% of the S&P 500 as of March 30, 2026. Investors who also own Nasdaq funds, growth ETFs, or individual mega-cap tech stocks may have even higher exposure.

Should retirees sell technology stocks before earnings?

Not automatically. The better move is to measure total exposure, run a 25% drawdown test, and make sure near-term withdrawals are not dependent on selling volatile equities. Retirees with oversized mega-cap tech positions may consider trimming back to a target allocation.

What should long-term investors do if they are still accumulating?

Investors with 10 or more years before retirement may be better served by staying disciplined, contributing on schedule, and rebalancing periodically. Earnings volatility is less dangerous when there are no forced withdrawals and the time horizon is long.

What is the simplest test for whether my tech position is too large?

Ask this: if your largest technology holding fell 30% after earnings, would you still hold it? If the answer is no, the position is probably larger than your actual risk tolerance.