Search “best retirement ETF”, and you will find a dozen listicles recommending a dozen different tickers. VOO. VTI. SCHD. JEPI. BND. Each article presents its list with the same confidence, and almost none of them answer the question that actually matters: which retirement ETF is right for your age?

That is the problem. Not the ETFs themselves, but the assumption that the question has a single answer.

A retirement ETF for someone in their mid-forties who is still building wealth has a completely different job than a retirement ETF for someone who retired last year and is drawing down income. Treating those two situations as identical is how investors end up in the wrong vehicle for their specific age — holding growth exposure they cannot afford to wait out, or holding conservative positions that cost them a decade of compounding they needed.

This piece answers the question by age and stage. Three phases. Three different sets of criteria. And the three funds that belong in almost every retirement portfolio regardless of where you stand.

The Job of a Retirement ETF Changes as You Get Closer to the Money

Most retirement ETF coverage is built around a single question: which fund has the best returns? That framing is wrong for anyone within ten years of retirement, and it becomes increasingly wrong the closer to drawdown you get.

The right question is: what job does this ETF need to do at your age right now?

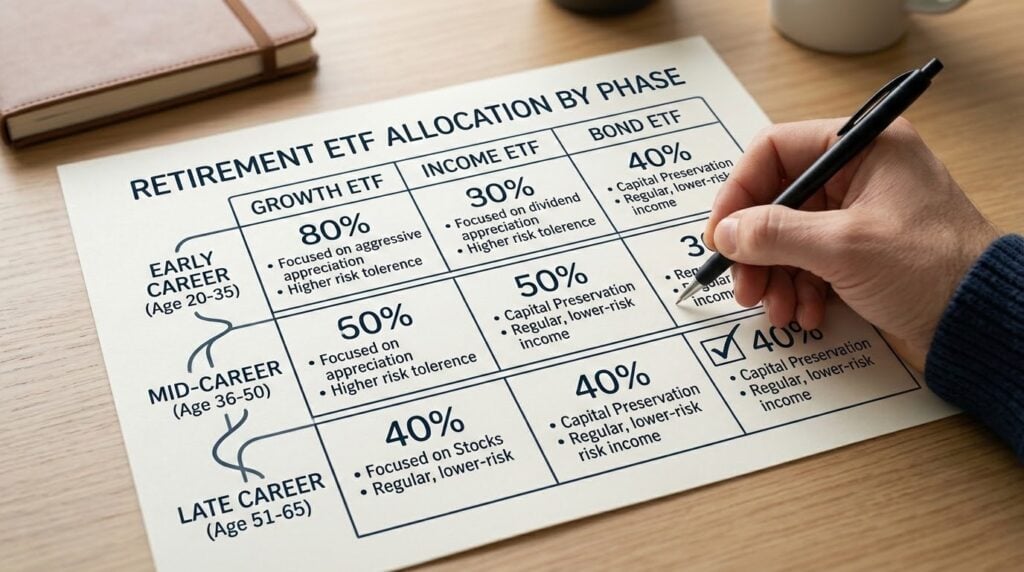

In the accumulation phase, when retirement is more than a decade away, the job is to grow capital at the lowest possible cost over a long time horizon. Volatility is manageable because time absorbs it. The investor who stayed in a broad market ETF through every correction in the last twenty years is ahead of nearly every tactical alternative, net of costs.

In the pre-retirement phase, roughly five to ten years out, the job shifts. The ETF portfolio now needs to grow while also building protection against a specific risk: a sustained market decline in the years immediately before retirement that forces the sale of equities at depressed prices to fund living expenses. Sequence-of-returns risk does its worst damage in this window. The ETF mix changes materially here even if the investor has not yet changed a single fund.

In the drawdown phase, when the investor is actively withdrawing, the job changes again. The portfolio exists to fund a distribution system. Income-producing ETFs earn their place here in a way they never fully justified during accumulation. The standard growth metrics that dominated the earlier phases matter less than yield, volatility, and the ability to generate cash flow without forcing equity sales during a down market.

These are not subtle differences in preference. They are structural differences in what the retirement ETF is actually being asked to do at each age.

The One Number That Matters Before Any Other

Before applying any phase-specific criteria, one number deserves to be the first filter on any retirement ETF candidate: the expense ratio.

Every basis point in annual fees is a guaranteed subtraction from return. It does not fluctuate with the market. It does not depend on fund manager skill. It compounds against the investor with mathematical certainty for as long as the fund is held.

The arithmetic is stark. A $100,000 investment growing at 7% annually for thirty years reaches approximately $761,000. The same investment in a fund charging 0.50% annually in fees reaches approximately $587,000. The difference of roughly $174,000 was never at risk in the market — it was guaranteed to the fund manager from the day the investor bought in. You can verify this calculation using the FINRA Fund Analyzer.

Broad market index ETFs hold expense ratios at or near 0.03% to 0.07%. The Vanguard S&P 500 ETF charges 0.03%. The Vanguard Total Stock Market ETF charges 0.03%. The Vanguard Total Bond Market ETF charges 0.03%. Thematic ETFs, actively managed ETFs, and many sector-specific ETFs regularly charge 0.50% or more.

The screening process for any retirement ETF starts here, before performance, before yield, before any other criterion. No fund that charges above 0.10% for broad market exposure passes the first filter. This rule eliminates a large portion of the ETF market before any further analysis is required.

The Accumulation Phase: What to Own in Your 40s and Early 50s

For investors more than ten years from retirement, the retirement ETF question is largely solved by three funds and a single discipline.

The three-fund structure consists of a total US market ETF, a total international equity ETF, and a total bond market ETF. Held together in proportions that match the investor’s age and risk tolerance, automated with regular contributions, and left alone through market cycles, this structure outperforms tactical and actively managed alternatives in the substantial majority of historical periods once costs are accounted for.

The specific funds that most consistently meet these criteria are the Vanguard Total Stock Market ETF (VTI, 0.03%), the Vanguard Total International Stock ETF (VXUS, 0.07%), and the Vanguard Total Bond Market ETF (BND, 0.03%). The iShares Core S&P 500 ETF (IVV) and SPDR S&P 500 ETF Trust (SPY) are functionally equivalent to VTI for the US equity component, though SPY’s 0.09% expense ratio is modestly higher.

One point worth noting for the accumulation-phase investor: US equity markets are trading at historically elevated valuations. The Shiller CAPE ratio, which measures current prices against ten years of average earnings, sits well above its long-run historical average. A retirement ETF portfolio that holds 100% US equity exposure is concentrated in one of the most expensive equity markets in recorded history. The total international ETF allocation is not a prediction that international markets will outperform. It is a structural hedge against the concentration risk that comes with a US-only position at current prices.

This is not a reason to abandon the accumulation doctrine. It is a reason to make sure the international allocation is not an afterthought.

The Pre-Retirement Phase: Shifting the Mix in Your Mid-50s to Early 60s

For investors five to ten years from retirement, the most important ETF decision is not which fund to add. Instead, it’s knowing which risk isn’t worth ignoring.

The specific risk is this: a 30% equity market decline in the two years before retirement, combined with a need to sell equity ETFs to fund living expenses, can permanently impair a retirement portfolio in a way that the same decline at age 40 never would. At 40, the investor has time and ongoing contributions working in their favor. At 60, they do not.

The pre-retirement ETF adjustment is about building the structure that prevents that scenario before the scenario arrives.

The equity ETF, VOO, VTI, or equivalent, belongs only in the portion of the portfolio that will not be touched for ten or more years. A Vanguard S&P 500 ETF that will fund expenses next year is not a ten-year holding. It is a near-term liability sitting in a volatile instrument.

Near-term expenses should be moving progressively toward a short-duration bond ETF. The Vanguard Short-Term Bond ETF (BSV, 0.04%) and the Vanguard Short-Term Government Bond ETF (VGSH, 0.04%) both provide low volatility and capital preservation for funds that will be needed within the next three to five years. These are not exciting holdings. That is the point.

A dividend ETF begins earning its place in the pre-retirement phase as a transition between pure growth and pure income. The Schwab US Dividend Equity ETF (SCHD) tracks approximately 100 dividend stocks with ten or more years of consecutive dividend growth and currently yields approximately 3.5% to 3.8% with an expense ratio of 0.06%. It provides income without fully abandoning equity upside, which makes it a natural bridge between the accumulation and drawdown phases.

The investor who arrives at retirement with two years of living expenses in cash or short-duration bond ETFs, a mid-range dividend ETF generating income, and a long-horizon equity ETF that is genuinely not needed for a decade is structurally protected against the single worst sequence-of-returns scenario. The one who arrives with 100% of savings in VOO is not.

The Drawdown Phase: Funding the Distribution System at 65 and Beyond

For investors actively withdrawing from their retirement portfolio, the ETF portfolio has one job: generate reliable income and capital preservation without forcing the sale of equity during a market decline.

Two types of retirement ETFs earn their place in this phase in a way they never fully justified during accumulation.

- The first is a dividend-focused equity ETF. SCHD yields approximately 3.5% to 3.8% at an expense ratio of 0.06% and generates cash flow from dividend payments rather than requiring the sale of underlying shares. The Vanguard High Dividend Yield ETF (VYM, approximately 2.8% yield, 0.06% expense ratio) covers a broader set of dividend payers across more than 400 holdings. Both provide income with significantly lower volatility than a pure growth equity ETF and avoid the forced-sale problem that makes a down market devastating for a retiree holding only growth positions.

- The second is a short-duration bond ETF. BSV and VGSH both serve as the near-term capital preservation layer, providing a source of withdrawals that does not require touching the equity positions during a market correction. The objective is to have enough in short-duration bonds that a two-year market decline does not force a single equity sale.

One structural point worth naming directly: covered call ETFs have become popular among retirees seeking high yields. JPMorgan Equity Premium Income ETF (JEPI) yields approximately 8% through a combination of large-cap stocks and S&P 500 options. The yield is real. The diversification is not always what it appears. A retiree who holds 50% of their portfolio in VOO and 50% in JEPI is, to a significant degree, holding the same underlying stocks twice — once for growth and once translated into yield. If US large-cap technology stocks undergo a sustained correction, both positions decline together. The income does not insulate the portfolio the way a bond ETF or international dividend ETF would.

International dividend ETFs address this in a way the covered call structure does not. The Schwab International Dividend Equity ETF (SCHY, approximately 3.2% yield, 0.14% expense ratio) provides geographic diversification alongside income, and international developed market equities currently trade at significantly lower valuations than their US counterparts. For the drawdown investor who cannot absorb a prolonged US equity correction, the international allocation adds a layer of structural resilience that a covered call ETF on the S&P 500 does not provide.

If you want to go deeper on the data behind why consistent, low-cost investing in a simple ETF structure outperforms timing and selection across nearly every historical period, the most rigorous case we have found is in Nick Maggiulli’s Just Keep Buying.

Disclosure: This article contains affiliate links. If you purchase through these links, TheCapitalist.com may earn a commission at no additional cost to you. See our affiliate disclosure policy.

The 3 Retirement ETF Plans That Belong at Every Age

Regardless of which phase applies, three retirement ETFs appear consistently across every well-constructed portfolio.

VOO or VTI provides the foundational US equity exposure at the lowest available cost. The question for most investors is not whether to own it but how much and in which part of the portfolio. During accumulation, it is the core holding. During the pre-retirement and drawdown phases, it belongs only in the long-horizon portion that will genuinely not be touched for a decade or more.

BND provides the sequence-of-returns buffer. Its role grows as retirement approaches. A 40-year-old might hold 10% in BND. A 60-year-old approaching retirement might hold 30% to 40%. The fund’s 0.03% expense ratio makes it the cheapest available source of bond market diversification, and its broad coverage of US government, corporate, and mortgage-backed securities provides genuine fixed income exposure rather than a narrow slice of the bond market.

VXUS provides valuation diversification. US equity markets are historically expensive relative to international peers. Holding a meaningful allocation in VXUS — not a token 5%, but a genuine 20% to 30% of the equity portion — reduces the structural concentration risk that comes with a US-only retirement ETF portfolio at current market prices. The fund’s 0.07% expense ratio keeps the cost minimal while covering over 8,000 non-US equity holdings across developed and emerging markets.

Together, these three retirement ETFs held in proportions appropriate to the investor’s age provide a foundation that the large majority of more complex alternatives fail to beat net of costs over sufficiently long periods.

For educational purposes only. Not financial advice. Consult a licensed financial professional before making investment decisions.

Frequently Asked Questions

What is the best retirement ETF for someone close to retirement?

For investors within five years of retirement, the priority shifts from growth to sequence-of-returns protection. A short-duration bond ETF such as BSV or VGSH combined with a dividend ETF such as SCHD or VYM provides income without requiring equity sales during market downturns. Keep broad equity ETF exposure in VOO or VTI only in the portion of the portfolio that will not be touched for ten or more years.

Is VOO a good retirement ETF?

VOO is one of the most cost-efficient ways to own broad US equity exposure, with an expense ratio of 0.03%. It is appropriate for the long-horizon growth portion of a retirement portfolio. It is not a complete retirement solution on its own. A retiree holding 100% VOO with no bond or income ETF buffer carries full sequence-of-returns risk and no source of income that does not require selling shares.

How many ETFs do I actually need for retirement?

Three is sufficient for most investors. A total US market ETF, a total international ETF, and a total bond market ETF cover the major asset class exposures at minimal cost. Adding more ETFs frequently increases costs and complexity without meaningfully improving diversification. The investor who holds VTI, VXUS, and BND in appropriate proportions and contributes consistently over decades will outperform the majority of more complicated alternatives.

What expense ratio should I look for in a retirement ETF?

Target below 0.10% for any broad index ETF. The difference between a 0.03% and a 0.50% expense ratio compounds to approximately $174,000 in foregone returns on a $100,000 investment over thirty years at 7% average annual growth, as verified by the FINRA Fund Analyzer. Expense ratio is the only guaranteed number in any ETF. Everything else is a projection.

What is sequence-of-returns risk, and which ETFs protect against it?

Sequence-of-returns risk is the danger that a sustained market decline in the years immediately before or after retirement forces the sale of equities at depressed prices to fund living expenses. Short-duration bond ETFs such as BSV and VGSH and dividend ETFs such as SCHD and VYM reduce this risk by providing income sources that do not require selling equity during a downturn.

Is JEPI a good retirement ETF for income?

JEPI generates approximately 8% yield through large-cap stocks and S&P 500 options. A portfolio holding both VOO and JEPI is largely concentrated in the same underlying US large-cap stocks. In a sustained US equity correction, both positions decline together. An international dividend ETF such as SCHY provides income with genuine geographic diversification that JEPI does not.