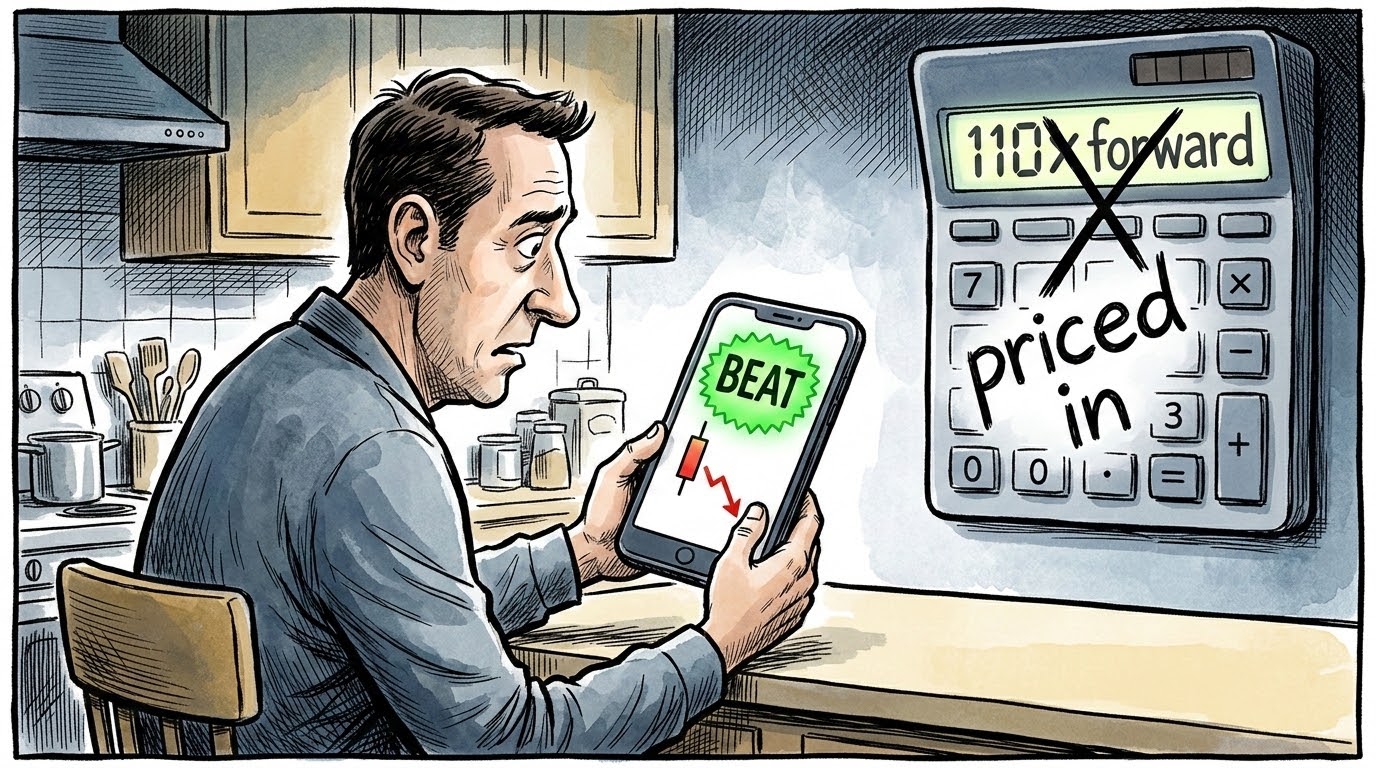

QUICK SUMMARY: Palantir reported Q1 2026 revenue of $1.63 billion, up 85% year over year. Adjusted EPS came in at $0.33 against a $0.28 estimate. The full-year guide was raised to $7.65 billion. Palantir stock fell roughly 3% on the print despite the clean beat. At 110x forward earnings, the market had already priced the beat in.

Palantir Q1 2026 landed Monday after the bell with a print that should have ripped the stock higher. Revenue grew 85% year over year, the fastest pace since 2020. Adjusted earnings per share beat by 18%. The full-year guide moved up by nearly $400 million. By every metric retail investors usually look at, this was the quarter Palantir bulls have been waiting for.

The stock fell anyway.

If you held PLTR into the print and you’re staring at red on your phone this morning trying to figure out what just happened, you’re not crazy. You’re learning a lesson about valuation that every retail investor eventually pays for. I paid for it twice before I figured out what the multiple was actually telling me.

The Print That Was Supposed To Move The Stock

Palantir’s Q1 2026 print delivered $1.63 billion in revenue (+85% YoY), an 18% EPS beat, and a $400 million raise to full-year guidance, yet the stock fell about 3%.

The numbers are objectively strong. Revenue of $1.63 billion beat the $1.54 billion consensus. Adjusted EPS of $0.33 cleared the $0.28 estimate by 18%. Net income roughly quadrupled year over year to $870.5 million. Q2 revenue guidance came in at $1.80 billion, well above the $1.68 billion Wall Street was modeling. Full-year guidance jumped to $7.65 billion, up nearly $400 million from the prior range.

The U.S. government segment was the standout. Government revenue accelerated to 84% year-over-year growth, up from 66% the previous quarter. The U.S. commercial customer count climbed from 375 in 2023 to 1,007 by Q1 2026. The CEO’s letter to shareholders called the results “a level of strength that dwarfs the performance of essentially every software company in history at this scale.”

Palantir stock fell about 3%.

There’s a comment that’s been kicking around investor forums for years that explains the disconnect better than any analyst note: “Beating estimates is easy. Most companies do that all the time.” The retail anger at the post-earnings drop assumes the beat is the whole story. The market thinks the beat is the floor.

Why A Clean Beat Still Lost

Palantir stock fell because at 110x forward earnings, the multiple had already priced in a beat-and-raise outcome before the print landed.

Palantir trades at roughly 110x forward earnings. To put that in context, Nvidia trades at about 30x. Datadog sits in the mid-50s. CrowdStrike is in the mid-70s. The closest peer to Palantir’s multiple is Snowflake at around 180x, and Snowflake is decelerating faster than Palantir.

At 110x forward, the bar isn’t “beat consensus.” The bar is “beat by enough to justify a higher multiple than 110x.” Run the reverse math. A forward P/E that high implies a five-year free cash flow growth rate sitting above the 95th percentile of historical software industry outcomes. That’s not unprecedented. It’s just rare. And it’s already in the price.

When the print landed, the beat was good enough to justify the multiple. It wasn’t good enough to expand it. Palantir stock fell because the math at this valuation requires beats to keep getting bigger, not just to keep happening.

This is what people mean when they say something is “priced in.” It’s not that the news doesn’t matter. It’s that the news has to be better than what the multiple already assumes. At 110x, the assumption bar is high enough that even a great quarter can land flat.

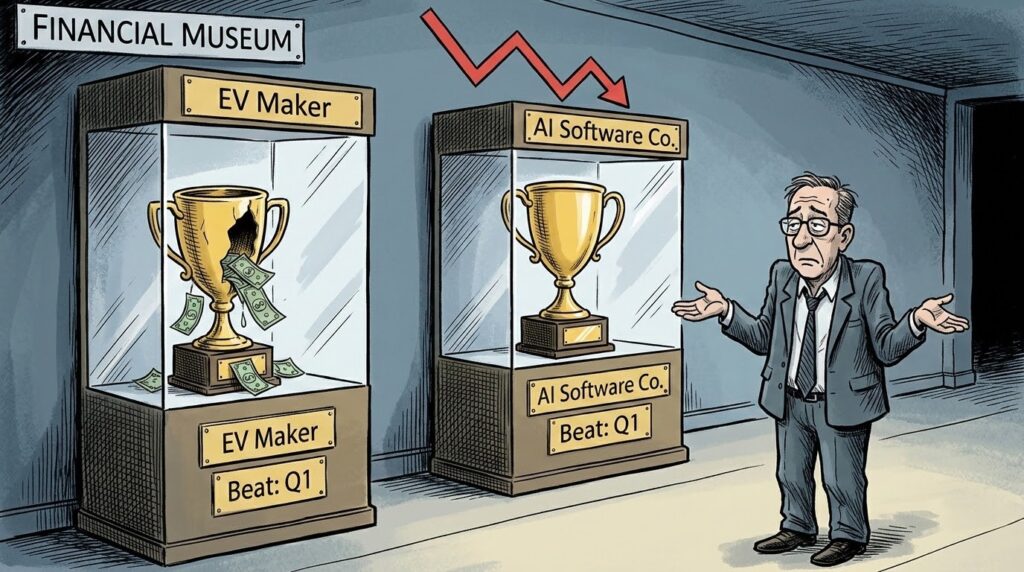

Why The Tesla Comparison Matters

Tesla’s Q1 beat was hollow and Palantir’s was clean, but both stocks fell because the multiple had already priced in the win in both cases.

Tesla beat earnings on Q1, too. The company’s profit was driven by undisclosed one-time benefits the CFO refused to size. Capex guidance jumped $5 billion. Free cash flow was guided negative for the coming quarters. The composition of the beat was hollow.

Palantir’s beat is the opposite. Revenue is genuinely accelerating. The guide is genuinely raised. No one-time accounting items are doing the heavy lifting. The print is clean.

Both stocks fell.

That’s the lesson worth carrying. When the multiple has already priced in the win, the composition of the beat is secondary. A hollow beat at Tesla’s 172x forward and a clean beat at Palantir’s 110x forward lose the same way. The mechanism is different. The result is the same. The math at extreme multiples doesn’t care whether your beat was real or accounting.

The Trap Behind The Last Rally

Last quarter Q4 2025, Palantir posted 70% YoY revenue growth and beat EPS by nearly 39%. The stock fell 11.62% the next day. This quarter the beat was smaller in percentage terms, and the drop was smaller. Same direction. Same lesson.

Palantir has now fallen on two consecutive earnings beats, confirming the multiple is driving the post-print move, not the print itself.

The trap is that retail holders remember the rallies and forget the post-beat compressions. The brain wants to believe the next beat will rally because some past beat rallied. That’s not analysis. It’s pattern-matching to the wrong dataset.

The honest pre-earnings question to ask, before any print on a stock at 100x+ forward: what probability would you assign to the stock falling on a clean beat? If your number is below 30%, you’re anchored on a prior rally. The market is telling you 30% to 40% is closer to the right answer. Two consecutive Palantir prints have now confirmed it.

Four Positions In Palantir Stock, Four Different Answers

The right move on Palantir stock depends on existing position size, time horizon, and proximity to retirement, not on the headline beat.

Palantir stock isn’t one decision. It’s four, depending on where you’re sitting.

- No position, considering entry. This print isn’t an entry signal. A beat-and-raise quarter wasn’t enough to clear the multiple. There’s no margin of safety in the numbers at 110x forward. Waiting costs nothing. Buying costs the full premium on a story that has to keep accelerating to defend the price.

- Position at or below target weight, long horizon. Hold. The print was clean. The business is genuinely accelerating. Single-print reactions are noise at the position-sizing level. Don’t add on the dip. Don’t sell on the news. The question is whether you would build the same allocation from cash today. If yes, hold. If no, the answer is rebalancing, not Q1.

- Position above target weight, compounded into concentration. This is the most common situation for anyone who held PLTR through 2024 and 2025. Rebalance to target. The decision isn’t whether the stock goes up next quarter. It’s what percentage of your equity exposure should sit in any single name at 110x forward earnings. For most disciplined retail portfolios, that number is somewhere between one and five percent. Above that range is the rebalance trigger.

- Within five years of retirement or already drawing income. Single-stock concentration at this valuation is a structural threat to your retirement plan, regardless of conviction in the AI thesis. The first years of drawdown are the most dangerous period of any retirement. A position that could realistically drop 40% to 60% in that window should not be sized to materially affect your income plan. This isn’t about picking a side on Palantir’s AIP. It’s about what your portfolio can survive if the thesis takes longer to play out than the market currently assumes.

For readers wrestling with the position-sizing question at extreme multiples, one book remains the cleanest informational reference for systematic discipline in a market that keeps rewarding narrative over math. The framework has been the counterweight to premium-multiple thinking for fifty years.

Disclosure: TheCapitalist may earn a commission from purchases made through links in this article. This does not influence our editorial coverage. See our editorial standards.

The Bottom Line

Palantir stock didn’t fall because the company is failing; it fell because the multiple had already priced in the win.

This isn’t a sell call. It isn’t a crash call. It’s a discipline call. Growth rates are forecasts. Multiples are facts. The price you pay for a story is the only thing you control after you click buy. At 110x forward earnings, what you’re buying isn’t the business as it is today. It’s the business as the multiple already assumes it will be in five years. Those are not the same purchase.

For educational purposes only. Not financial advice.

Frequently Asked Questions

Why did Palantir stock fall after a Q1 earnings beat?

Palantir traded at roughly 110x forward earnings going into the print. At that multiple, the market had already priced in a beat-and-raise quarter. The stock fell because the beat met expectations rather than exceeding them by enough to justify further multiple expansion.

What were Palantir’s Q1 2026 earnings results?

Palantir reported revenue of $1.63 billion, up 85% year over year, beating the $1.54 billion consensus. Adjusted EPS was $0.33 against a $0.28 estimate. Full-year revenue guidance was raised to $7.65 billion, up from the prior $7.18 billion to $7.20 billion range. U.S. government revenue accelerated to 84% year-over-year growth.

How does Palantir’s valuation compare to other AI stocks?

Palantir trades at approximately 110x forward earnings. Nvidia trades at roughly 30x. Datadog sits in the mid-50s and CrowdStrike in the mid-70s. The closest peer at this multiple is Snowflake near 180x, though Snowflake is decelerating faster than Palantir.

Should I buy Palantir stock after the Q1 drop?

The answer depends on existing position size, time horizon, and proximity to retirement. At this valuation, there is no margin of safety in the numbers. Investors with no position face an entry decision with limited downside protection. Investors with concentrated positions should review whether the current weight matches their target portfolio allocation.