Rate cut expectations pointed one way at the start of 2026. Investors came into the year betting on one or two cuts, and built portfolios around them. Going into the June FOMC meeting on June 16 and 17, those bets have all but disappeared. Futures markets now price a near-certain hold, leaving the target range at 3.50 to 3.75 percent. The decision lands at 2 p.m. ET on June 17, and it will be one of the first as chair for Kevin Warsh, who took over from Jerome Powell in May.

The market has stopped expecting help. The question is whether your portfolio still expects it.

What Killed Rate Cut Expectations

The short answer is that inflation came back. April prices rose 3.8 percent from a year earlier, pushed up by an energy shock tied to conflict in the Middle East. Core inflation is still sitting near 3 percent, well above the 2 percent goal. A central bank does not cut into rising prices, so the cuts are off the table for a good reason, not a bad one.

The big banks have already moved. JPMorgan now sees zero cuts this year and pencils in a hike for 2027. Bank of America has pushed its first cut all the way out to July 2027, a call we covered when it moved its forecast. This follows a string of holds that we tracked back in late April, and a leadership handoff that began with. Powell’s last meeting and a new chair whose stance the market is still reading. The May jobs report on June 5 and May inflation on June 10 are the last data points before the FOMC decides.

Bottom line: futures price is a near-certain hold at 3.50 to 3.75 percent, with no cut expected at the June 17 decision.

The Trades That Ran on Cheap Money Will Reprice First

Here is why this matters beyond the headline. When the market expected rates to fall, money flowed to the bets that gain the most from cheaper borrowing: the longest, the riskiest, the furthest from current profits. Take away the cut, and those same bets give the most back. The repricing is not random. It starts at the speculative edge and works inward.

You can hear the strain in how investors are talking. One reader summed up the paralysis in four words: “I feel stuck sitting in t-bills.” Sitting in cash felt safe while everyone waited for the Fed to move. Now the wait has no end date, and the holding pattern itself has a cost.

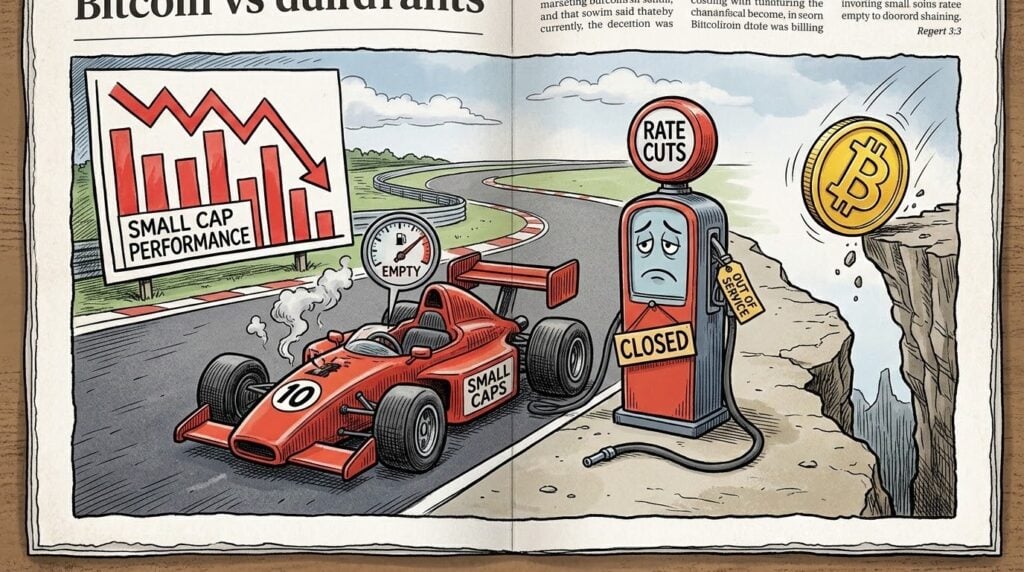

The Small Cap Rotation Was a Bet on Earlier Rate Cut Expectations

The clearest example is small caps. The Russell 2000 spent months leading the market, breadth climbed to multi-year highs, and roughly 65 percent of small companies beat their latest earnings, the best showing since 2021. Small caps still trade at about a 31 percent discount to large caps. On paper, that looks like a setup.

But the small-cap rotation leaned heavily on one assumption: falling rates and a steeper yield curve. Smaller companies carry more floating-rate debt and feel rate moves faster, so the trade was, in large part, a bet on cuts. With the cuts gone, the main support beam is weaker. The discount is real, but a discount that only works because rates were going to drop is not a discount for the right reason. Before adding here, price these companies against a world where rates stay put, not the one that was promised in January.

Key risk: the roughly 31 percent small-cap discount assumes falling rates, so it means less if rates stay where they are.

Risk-Off Is Hitting the Speculative End Hardest

The other place the repricing shows up is the speculative end, and crypto is the loudest example. Bitcoin slid below 70,000 dollars for the first time since April, down about 6 percent in a day and roughly 45 percent below its October peak near 126,000 dollars. The bigger tell is where the money is going. Spot bitcoin funds saw about 4.21 billion dollars in withdrawals over three weeks, the largest stretch of outflows this year. The institutions that were supposed to be the steady buyers are the ones heading for the door, and sentiment readings now sit in extreme fear.

None of this is a verdict on the long-term case for digital assets, which we cover separately. Crypto is volatile and can lose value quickly, and it is not suitable for money you cannot afford to lose. The point is narrower: assets that ran on loose-money optimism are the first to reprice when that optimism drains. As one market commentator put it, if you are betting on a Fed pivot to bail out your portfolio, don’t.

Long Horizons Tune It Out, Short Horizons Reposition

So what do you actually do. The honest answer splits on one thing, and it is not the Fed. It is your own clock.

If you are ten or more years from needing this money and still adding to it, the meeting is noise. The data on people who try to trade around Fed decisions is brutal: most end up trailing the very funds they hold, because they sell into fear and buy back into relief. Keep your automatic contributions running, hold your allocation, and let June 17 pass without touching anything.

If you are within three to five years of needing the money, or you know you would not sit calmly through a 40 percent drawdown, the regime now in front of you deserves a response. That does not mean selling everything. It means trimming the bets that only worked if rates fell, leaning toward quality and dividend payers over profitless growth, and using the fact that short-duration Treasuries and T-bills still pay a real yield while you wait. Cash is no longer a penalty box.

Across both paths, decide before the meeting, not in the hour after the statement drops. The investors who reposition on the print are the ones who get whipsawed.

The cut is not coming. The most useful move for most readers is to stop building a portfolio that needs one.

Disclosure: TheCapitalist.com participates in affiliate programs and may earn a commission if you buy through links in this article. This never influences our editorial coverage.

If the lesson here is that trying to time the Fed is a losing game, one resource makes that case in plain language. As an educational partner pick, the fiftieth anniversary edition of A Random Walk Down Wall Street by Burton Malkiel walks through why steady, low-cost investing tends to beat outguessing the next policy move, and the current edition adds chapters on cryptocurrencies and meme stocks that speak directly to this moment.

Frequently Asked Questions

Will the Fed cut rates at the June FOMC meeting?

A cut is not expected. Futures markets price a near-certain hold, leaving the target range at 3.50 to 3.75 percent. The bigger signal will be the updated projections and the new chair’s tone, not the rate itself.

Why is the Fed not cutting interest rates if inflation came down from its peak?

Inflation reaccelerated to 3.8 percent in April on an energy shock, and core inflation is still near 3 percent. Both sit above the 2 percent target. Cutting into rising prices risks re-stoking inflation, so the central bank is holding.

Are small-cap stocks still a buy if rates stay high?

They are cheap, with a near-31 percent discount, and earnings have been strong. But the rotation leaned on falling rates, so the question is whether the case still holds when rates do not drop. Judge each name on whether it works at today’s rate, not a lower one.

What should I do with cash while rates stay elevated?

Short-duration Treasuries, T-bills, and money market funds still pay a real yield, so cash is not the penalty it was a few years ago. The cost is opportunity if markets rebound. Match the amount to how soon you need the money.