QUICK SUMMARY: The US-China tariff reduction deal coming from the May 2026 Trump-Xi summit creates real tailwinds for semiconductors, consumer goods, agriculture, and emerging markets. But the market’s immediate gap-up has likely closed the entry window on at least two of those sectors. This analysis identifies which sectors still have runway and what most portfolios should actually do right now.

Markets priced in the US-China tariff reduction deal before the details were confirmed. Wall Street’s reaction is the first thing an investor needs to understand, because the gap between what was announced and what was actually agreed may be wider than the rally suggests. For investors, this is real news but is also incomplete news. And the gap between those two facts is what determines whether your next portfolio move makes money or costs it.

What Did the US-China Tariff Reduction Deal Actually Agree To?

The precise terms of the May 2026 summit agreement are still being worked out. What has been confirmed is a preliminary commitment to further tariff reductions and expanded agricultural market access, corroborated by four independent wire services within a 48-hour window.

That pattern should be familiar. The US and China have run four successive rounds of tariff negotiations since April 2025. The original 90-day truce in May 2025 cut the US effective tariff rate on Chinese goods to 17.8%, a reduction of more than 10 percentage points, according to a Yale Budget Lab analysis. That truce extended in August 2025, again after the October 2025 Busan summit, and again through early 2026. Each round produced market-moving headlines. None produced a formal signed agreement.

As traders priced it before the Beijing summit, the probability of a formal agreement being completed by May 31 sat at 44.5%. “Extensions are not agreements. Rollovers are not deals. The deadline is hard.” The market gapped up anyway.

The second federal court ruling that the Trump tariffs were illegal earlier this year adds another layer of legal uncertainty to any preliminary deal framework. Here is what the current context means for the four sectors with real exposure.

Which Sectors Benefit Most From the US-China Tariff Reduction Deal?

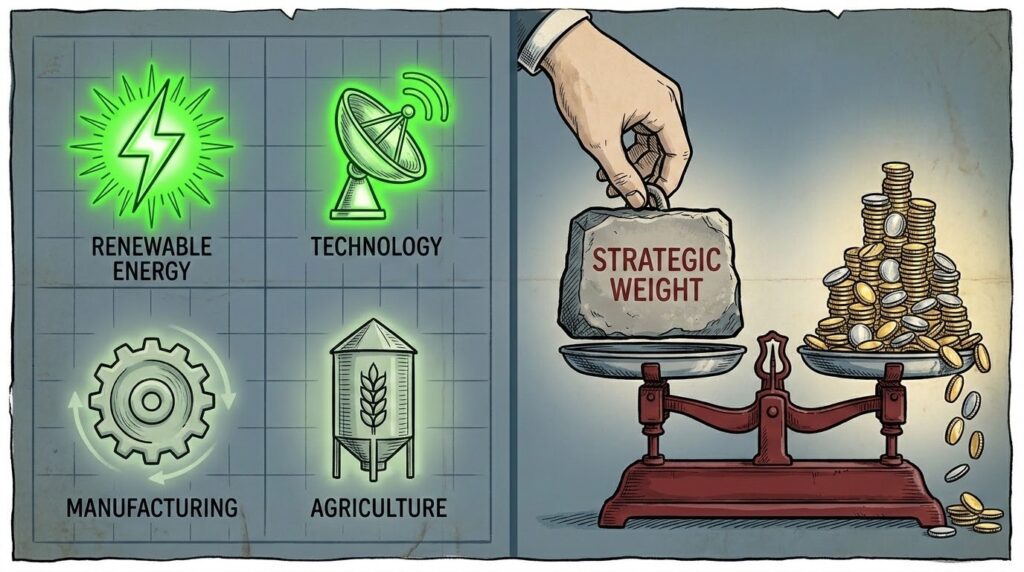

Four sectors have direct exposure to the deal. They are not equal. Two have a durable structural case that holds whether the preliminary agreement formalizes or extends again. Two are priced for a resolution that has not yet been signed. The distinction matters more than the sector list.

Semiconductors

Chipmakers with meaningful China revenue concentration have the most direct exposure to any tariff reduction. When the May 2025 truce was announced, the iShares Semiconductor ETF (SOXX) gained 6.7% on the announcement day alone. The sector logic is direct: lower tariffs reduce input costs and remove the regulatory uncertainty that has depressed capital allocation in the sector since early 2025.

The question investors need to answer before acting is whether that re-rating has already happened. The Magnificent 7 added $837.5 billion in combined market cap on the day the May 2025 deal was announced. The investors who captured the initial rally gains were already positioned before the headline hit. Before adding semiconductor exposure, confirm whether the current price still reflects a tariff discount or whether the discount has already been removed by the initial gap-up. For a deeper look at the valuation math specific to chips, see Should You Buy Semiconductor Stocks at Current Valuations?

Consumer Goods and Retail

Retailers and consumer brands importing from China got a direct cost relief catalyst. Amazon gained 7.4% on the May 2025 truce announcement. Companies importing manufactured goods from China faced meaningful margin compression under elevated tariff regimes. Reduced duties are a real tailwind on input costs, at least for the duration of the current truce window.

The same valuation warning applies here. “Stocks are ripping higher after news of a U.S.-China trade deal, but will it last?” was the question analysts were asking the morning after the May 2025 announcement. Buyers entering consumer goods positions after a significant gap-up are pricing in a formal deal that carries a 44.5% probability of completing by month’s end.

Agriculture

Agriculture has the most durable investment case of the four sectors because its structural support extends past the deal’s 90-day window. China is the largest international market for US soybeans, cotton, and meat. Agricultural exports represent 20% of US farm income according to the American Farm Bureau Federation. The October 2025 Busan agreement specifically named resumed Chinese purchases of US soybeans as a committed action item. That precedent is now active. The May 2026 preliminary agreement includes expanded agricultural market access, building on trade flows that have already resumed.

Deere gained 5.5% and ADM gained 5.9% on the May 2025 truce. Agricultural trade normalization has structural political support in both Washington and Beijing. This sector’s investment case holds even if the formal agreement slips past the May 31 deadline, which is not true of semiconductor or consumer goods positions priced at full value.

Emerging Markets

This is the sector where the investment case extends furthest beyond the specific deal. Emerging market equities outperformed the S&P 500 in 2025 despite the trade war, driven by AI adoption in China and semiconductor weightings in the MSCI EM Index, according to Charles Schwab’s 2026 international outlook. China’s 15th Five-Year Plan, covering 2026 through 2030, targets investment in semiconductors, industrial machinery, high-end equipment, and advanced materials. That structural bid exists independent of whether the May 2026 preliminary agreement formalizes or extends again.

A deliberate emerging market allocation is not a tariff-deal trade. It is a geographic diversification decision supported by earnings re-rating and structural policy investment that predates this summit. For specific ETF instruments, see our guide to emerging market investing during US stock volatility.

This article contains affiliate links. If you purchase through these links, TheCapitalist.com may earn a commission at no additional cost to you.

For investors who want to understand what the data shows about consistent accumulation into diversified global markets through periods of geopolitical volatility, Just Keep Buying covers that research in full detail.

The Capitalist may earn a commission on books purchased through links below, at no cost to you.

Has the Stock Market Already Priced In the US-China Tariff Reduction Deal?

Here is the uncomfortable math. The Mag 7 added $837.5 billion in market cap in a single session when the May 2025 truce was announced. SOXX gained 6.7%. Amazon gained 7.4%. Markets price major macro catalysts in hours.

J.P. Morgan’s analysis of that deal noted that the magnitude of the tariff reduction was larger than expected and that further gains were possible. Morgan Stanley’s read one month later was more cautious: following the de-escalation with China, further reductions looked less likely. Both were right. The initial rally had legs. The second-order gains were slower and more selective.

One additional indicator is worth tracking in the days after this summit: the 10-year Treasury yield. If yields rise sharply, the bond market is pricing out Federal Reserve rate cuts in response to reduced trade-driven deflation pressure. That puts a ceiling on how far the sector rally extends. For context on how the Fed rate hold has already reshaped bond positioning in 2026, see Fed Rate Hold Extends to a 3rd Consecutive FOMC Meeting.

Should You Buy Stocks After the US-China Tariff Reduction Deal?

A straightforward position, held by a large share of long-horizon index investors, is that none of the above analysis should change anything. The truce infrastructure has rolled over three times without a formal agreement. The deal is preliminary. The formalization deadline is two weeks away. And for an investor holding a broad global index fund, the US-China tariff reduction deal is already embedded in the portfolio. When Chinese equities rise, so does the emerging market allocation in a total world fund.

“Or, you could, you know, not try to time the market,” was the blunt summary from one Bogleheads forum member during the tariff volatility of early 2025. It was not wrong. For the long-horizon accumulation investor, the correct and complete response to this deal is mechanical: trim the equity overweight the rally created back to strategic weight and return to the regular contribution schedule.

“The strategic rivalry remains. The truce is tactical.” That assessment from a cross-border trade analysis published in February 2026 has not been invalidated by the Beijing summit. It has been confirmed.

How Should You Rebalance Your Portfolio After the US-China Tariff Deal?

Three moves, mapped by investor type.

For the broad accumulation investor: trim the equity overweight the rally created. If your target is 80% equity and the gap-up pushed you to 83%, bring it back to 80%. That is the trade. Nothing more is required.

For the active allocator with existing China-sector exposure: run an implied risk premium check on semiconductor and consumer goods positions before adding. If the tariff discount has already normalized, wait for the next tariff headline to create a new entry point.

For any investor currently underweight emerging markets, this is the one area where the investment case extends past the specific deal timeline. China’s five-year plan, the EM earnings re-rating cycle, and the structural shift in global tech supply chains all support a deliberate EM allocation that holds whether this particular US-China tariff reduction deal formalizes in two weeks or extends for another 90 days.

For long-horizon index investors, the US-China tariff reduction deal is already embedded in a broad global fund — no action required beyond trimming any overweight the rally created.

For educational purposes only. Not financial advice. Consult a licensed financial professional before making investment decisions.

Frequently Asked Questions:

Which sectors benefit most from the US-China tariff reduction deal?

The four sectors with the most direct exposure are semiconductors, consumer goods and retail, agriculture, and emerging markets. Agriculture and emerging markets have the most durable cases because both are supported by structural factors that extend beyond the deal’s 90-day window. Semiconductor and consumer goods gains are more directly tied to whether the preliminary agreement formalizes and whether the initial valuation re-rating has already been fully priced in.

Has the stock market already priced in the US-China tariff reduction deal?

Partly. When the May 2025 truce was announced, the Mag 7 added $837.5 billion in market cap in a single session and the iShares Semiconductor ETF gained 6.7%. Markets price major macro catalysts in hours, not days. Semiconductor and large consumer goods names that gapped on the original announcement are likely fully priced at current levels. Agriculture and emerging market exposure may still offer runway because their investment cases extend past the truce window itself.

Should I add semiconductor stocks after the US-China tariff reduction deal?

Only after checking whether the tariff discount has already been priced out. Compare the sector’s current implied risk premium against the pre-tariff baseline from early 2025. If the premium has normalized, the entry window created by this deal has closed and new buyers are paying full value on a preliminary agreement that carries a 44.5% probability of formalizing by May 31. If a meaningful discount remains, a selective position has a valuation basis.

What does the US-China tariff reduction deal mean for a long-term index investor?

For most long-horizon index investors, the correct response is mechanical. If the market rally pushed your equity allocation above your strategic target weight, trim it back to target. A broad global index fund already holds Chinese and emerging market equities at market weight, so the deal is already embedded in the portfolio. Adding sector tilts based on a preliminary agreement with a two-week formalization deadline is a reaction to a headline, not a portfolio decision.

What is the difference between a tariff truce and a formal trade agreement?

A tariff truce is a temporary, time-limited pause in escalation that both sides agree to honor while negotiations continue. A formal trade agreement is a signed, binding document. The US and China have operated under four successive truce extensions since May 2025. None has produced a signed agreement. The May 2026 preliminary deal follows the same pattern.

How did the May 2025 US-China tariff truce affect markets?

The May 2025 truce cut the US effective tariff rate on Chinese goods to 17.8%, down more than 10 percentage points, according to Yale Budget Lab data. The Magnificent 7 added $837.5 billion in combined market cap on the announcement day. The iShares Semiconductor ETF gained 6.7% and Amazon gained 7.4% in the same session.

Is the US-China tariff deal permanent?

No. The May 2026 agreement is preliminary and subject to a formalization deadline. As of the summit, analysts placed the probability of a completed formal agreement by May 31 at 44.5%. The pattern since April 2025 has been successive 90-day extensions rather than a permanent resolution.