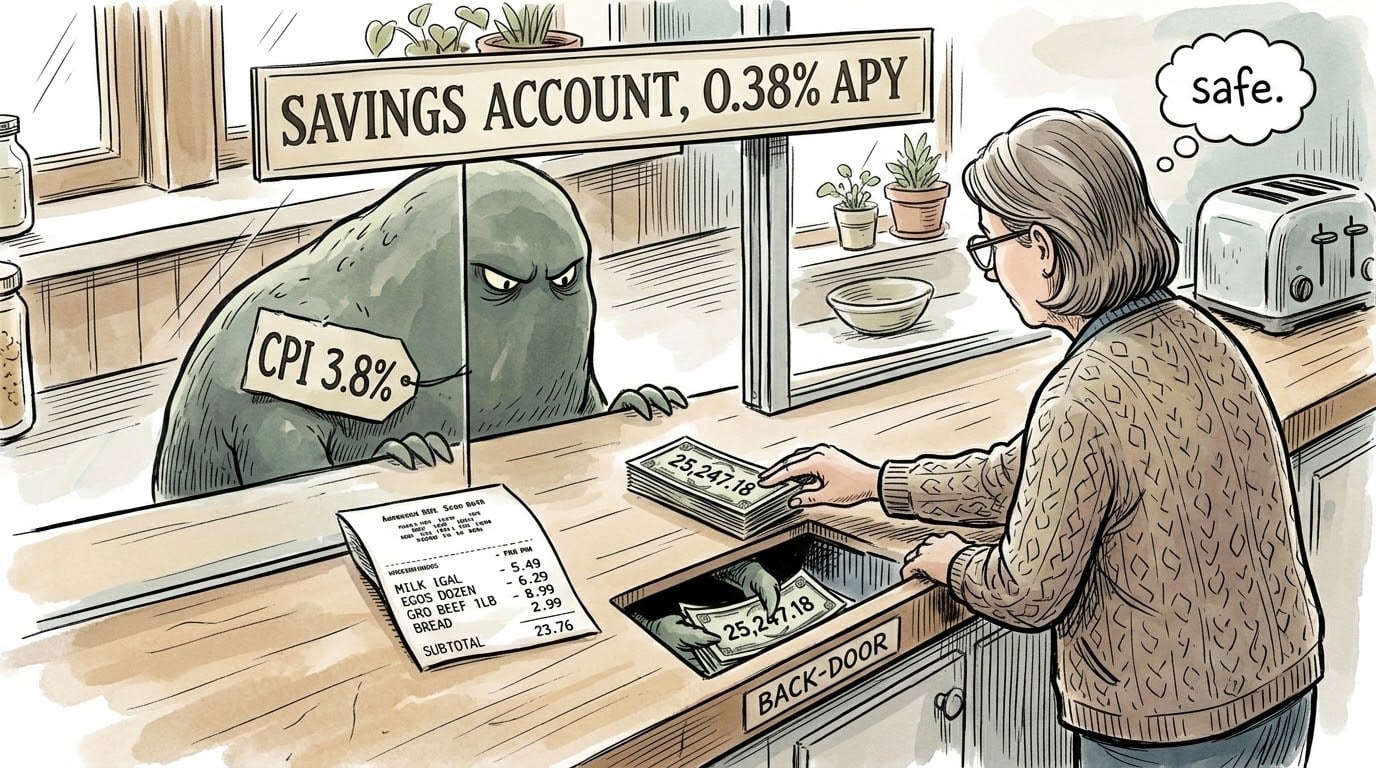

If you watched the April Consumer Price Index land at 3.8% and then checked your savings account balance the same week, you saw two numbers that no longer line up the way they used to. Inflation outpacing savings was supposed to be the 2022 story. It is back, and the spread between what your cash earns and what your cash needs to earn has just compressed to its narrowest level in three years.

The Bureau of Labor Statistics reported that the all-items Consumer Price Index, known as CPI, climbed 3.8% over the 12 months ending in April 2026. That print followed a 3.3% reading in March and a 2.4% reading in February. Inflation rose 140 basis points in two months, the steepest such climb in nearly three years. Wholesale prices showed an even sharper acceleration over the same window, and Wall Street has been recalibrating equity targets around the new regime.

Energy prices drove most of the move. The energy index rose 17.9% over the year, with gasoline up 28.4% annually, after the late February strikes on Iran reshaped global supply expectations.

On the other side of the math, the Federal Deposit Insurance Corporation reports that the national average savings account pays just 0.38% Annual Percentage Yield, often called APY. Top competitive high-yield savings accounts (HYSAs) sit between 4.00% and 5.00% APY as of June 2026, according to recent rate tracking from Bankrate and Fortune.

The gap is wider than most savers realize. At the national average of 0.38%, every $10,000 sitting in cash lost roughly $342 in real purchasing power over the past year. At a top-tier HYSA paying 4.00%, the same $10,000 ended the year with a real gain of about $20 before tax. That 20-basis-point cushion is the entire margin protecting cash from inflation right now.

At the bottom end of the table, the math turns ugly fast. A recent analysis put it plainly: at a typical big-bank rate of 0.01% APY, $10,000 earns about $1 of interest while simultaneously losing $380 of purchasing power.

The gap between the average savings account and the top-tier high-yield account is now 362 basis points, wider than the spread between top-tier and inflation itself.

A nominal balance that does not move while purchasing power does is a deliberate trade, not a default safe choice.

Inflation Outpacing Savings Is a 2026 Story, Not an Evergreen One

Inflation always erodes some cash value. Over the past century, that drag has averaged about 2% per year, the same number central bankers set as their long-run target. Savers have lived with it the way drivers live with tire wear. What changed in 2026 is the size of the gap and the speed at which it opened.

Two forces met in the middle. The Federal Reserve held rates steady through 2026 after cutting six times across 2024 and 2025. Those cuts pulled top HYSA APYs down roughly 100 basis points from their 2024 peaks. At the same time, inflation accelerated from 2.4% in February to 3.8% in April. The closing speed was almost symmetrical. Rates moved down. Inflation moved up. The cushion was halved in about 60 days. Major Wall Street forecasters have since pushed expectations for the next rate cut into 2027, extending the hold deeper than markets priced in earlier this year.

The structural argument runs deeper than the monthly print. Federal deficits remain elevated post-2024. Treasury issuance keeps climbing. The math of a government borrowing heavily while inflation runs above its rate target tends to compress real returns on cash for an extended stretch. Reading the deficit trajectory tells savers more about where real cash returns are heading than reading the next Fed statement.

The squeeze is not because banks got greedier. It is because the gap between what cash earns and what cash needs to earn closed from two sides at once.

Real return on savings is decided in Washington, not at your branch.

The Job Your Savings Account Is Designed to Do

There is a fix to this problem, but it starts with a definition that most savers skip past. A savings account is not supposed to beat inflation. It is supposed to give you cash you can reach in 24 hours without selling stocks at the wrong time. Those are not the same job.

A workable framework separates cash into two distinct horizons. The first holds one to two years of expected expenses in liquid accounts that prioritize availability over return. The second holds three to ten years of expected expenses in instruments that prioritize real return over availability. The first protects you from being a forced seller during a market downturn. The second hedges against the inflation creep that compounds over a decade. The two buckets exist to do different work.

On long-running personal finance forums, savers articulate this discipline themselves. As one frequent contributor put it: “No one is getting rich off the interest of their emergency funds. Their main job is not to work for you and grow, but rather to not lose value and to be appropriately liquid.” That framing matters because it shifts the question from “how much am I earning” to “how many months does this cover.”

The trap shows up when a near-term cash bucket gets confused with a long-term inflation hedge. The saver chases yield, switches banks every quarter, and still loses real purchasing power because the entire structure was built for a different job.

The wrong question is “How much am I earning on my savings?” The right question is “how many months of expenses does this cover?”

A 20-basis-point real return is the right return for a bucket that is supposed to insure you against bad timing, not generate wealth.

When Cash Is Insurance and When Cash Is a Slow Loss

Savers reading this far will notice an unresolved tension. If cash protects against bad timing in equities, but cash itself is losing purchasing power, when does the protection cost more than the risk it absorbs?

This is where the framework splits. One school argues that near-term cash buckets should be defended at all costs because the behavioral protection they offer, against panic-selling stocks at the bottom, is worth more than the inflation drag they incur. The other school argues that in expansionary fiscal regimes, holding meaningful cash is a guaranteed slow loss, and the better choice is a risk-balanced allocation across stocks, longer-duration Treasuries, commodities, and gold.

Both positions hold under different conditions. The reconciliation is keyed to your time horizon and your behavioral capacity, not to a one-size-fits-all rule.

For cash you might need in three years or less, and which represents emergency liquidity or planned near-term spending, the bucket discipline holds. Accept the real-return drag. Do not move the money. The optionality is what you are paying for.

For cash you can ringfence for three to ten years and which is meaningfully larger than your emergency liquidity, the answer splits. Short-duration Treasury Inflation-Protected Securities, known as TIPS, and Series I Savings Bonds (I-bonds) recover the inflation hedge while preserving principal stability. This approach works until purchase limits or lockup rules create a liquidity gap.

For cash that has been parked indefinitely as a “safe” long-term holding, the math turns against you. A cash position with a 10-year horizon is not safe in any meaningful sense. It is a slow withdrawal. The better move is a risk-balanced allocation across multiple asset classes.

A behavioral override sits across all three. If you cannot hold equities through a 40% drawdown without selling, keep the cash you can hold without panic. Inflation drag is a cheaper tax than panic-selling at the bottom of a bear market.

Optical stability is not actual stability. A balance that does not move while purchasing power does is a quiet decision to lose money.

The horizon decides the answer. Three years is bucket discipline. Ten is regime rotation.

Where the Inflation Hedge Actually Belongs

The instruments built to do the inflation-hedging job are not savings accounts. They are TIPS and I-bonds. Both come with constraints, and those constraints are the reason savers reach for HYSAs by default. The constraints are also why HYSAs cannot do the inflation-hedging job at all.

I-bonds are the most retail-accessible inflation hedge. They carry a 12-month redemption lockup from the date of purchase. Sell within five years and you forfeit the most recent three months of interest. Individuals can buy up to $10,000 of electronic I-bonds per calendar year through TreasuryDirect, plus an additional $5,000 from a federal tax refund. The interest accrues tax-deferred and is exempt from state and local income tax.

TIPS solve the purchase-limit problem at the cost of more day-to-day price volatility. A short-duration TIPS fund, accessed through tickers like VTIP or STIP, offers daily liquidity and unlimited capacity, but the principal can move with real-rate changes between purchase and sale. For Bucket 2 money you will not touch for five years, that volatility is largely irrelevant. For Bucket 1 emergency funds, it disqualifies the instrument outright.

The point of naming these tools is not to push a specific allocation. It is to make explicit that the inflation-hedging job has its own department. The savings account department was built for something else. Income-paying equity sleeves like real estate investment trusts sit in their own conversation and bring a different volatility profile again, but the bucket frame still applies.

On forums where pre-retirees discuss this trade-off, the framing arrives in plain language. As one poster wrote: “I do not want to lose to inflation. Which brings us to I bonds.”

The job of Bucket 1 is to hold value. The job of Bucket 2 is to beat inflation. Trying to do both in one account fails both.

I-bonds are a hedge, not a substitute. The 12-month lockup is the cost of admission.

Audit, Right-Size, Diagnose: The Three Moves Worth Making This Quarter

A saver can take three steps this quarter without rebuilding a portfolio. The first is an audit. The second is a resize. The third is a diagnosis.

Step one is to compare your current effective APY against the top-tier APY available. If you bank with a national institution paying 0.01% to 0.38%, the gap to a top-tier HYSA is 362 to 399 basis points. That gap is the actionable number. If you are already within 50 basis points of the top tier, stop bank-hopping. The marginal yield is no longer worth the behavioral cost or the paperwork.

Step two is to right-size your near-term cash bucket to your actual months of expenses, not to a portfolio percentage. The number that matters is months covered, not dollars held. A near-term bucket covering 36 months of expenses is too large. A bucket covering 1 month is too small. Most savers fall on one side or the other. Both create costs. Oversized cash incurs an inflation drag. Undersized cash creates the risk of forced equity sales during a downturn.

Step three is the diagnosis. The two failure modes look similar from the outside, but they call for opposite responses. Near-term bucket drag means too much cash sitting at a low APY. The fix is to move it to a top-tier HYSA or trim the bucket. A missing inflation hedge means no real-return protection anywhere in your plan. The fix is to add a position in TIPS or I-bonds for the longer-horizon money. The diagnosis decides which fix you reach for.

A recent wire analyst summarized the broader picture for households this cycle: “Today, there is little room to keep spending by saving less.” Americans are tapping savings to cover expenses while the cushion erodes from both ends. The fix is rarely a bigger search for yield. It is usually a clearer answer to the question of what each bucket is supposed to do.

The discipline that holds whether the spread is 20 basis points or 200 basis points is the same one that protects savers from a bigger mistake: over-managing the cash bucket while under-managing the rest of the portfolio. A Random Walk Down Wall Street by Burton G. Malkiel, now in its 13th edition, is the long-form case for cost discipline, behavioral consistency, and the argument against trying to forecast which corner of the market will win next. Our educational partner link is below.

[AAWP shortcode placement here — ASIN 1324035439]

Audit, right-size, diagnose. Three steps. None of them is “shop harder for yield.”

The answer to a narrowing spread is rarely a bigger search. It is usually a better question about what cash is for.

The Headline Will Move. The Structure Should Not.

Inflation outpacing savings will keep showing up in headlines as long as the fiscal and monetary forces driving it remain in place. The headline is not the action item. The action item is the diagnosis: which bucket is doing the wrong job in your plan, and what is the smallest change that fixes it. The spread will widen and narrow. The structure of how you hold cash is the part that protects you regardless.

For educational purposes only. Not financial advice. Consult a licensed financial professional before making investment decisions.

Frequently Asked Questions

If my high-yield savings account pays 4.00% APY and inflation is 3.8%, am I actually losing money?

At the nominal headline rate, no. At real terms before tax, you have a 20-basis-point cushion. After federal and state income tax on the interest, the real return is often negative for higher-income earners. The HYSA wins the headline race and loses the after-tax-after-inflation race for many savers.

Should I move my emergency fund into I-bonds?

It depends on the size of the fund and how you might need to access it. I-bonds carry a 12-month redemption lockup and a 3-month interest penalty for redemption within the first five years. If your emergency fund is large enough to layer, with part in an HYSA for immediate access and part in I-bonds for the 12-plus-month tier, splitting can work. If you might need all of it inside the first year, no.

How often should I check my savings APY?

Quarterly is usually sufficient. Variable APY accounts can move without notice, but bank-hopping more frequently than that becomes a behavioral drag for marginal yield. Set a calendar reminder for the same week each quarter and review it then.

What does the narrowing spread between top APY and inflation actually tell me right now?

A narrower spread does not mean abandoning cash. It means the cash bucket is working at the lowest margin in three years, so the size of that bucket matters more than ever. Savers with oversized cash positions are paying a larger drag tax than they were 18 months ago.